Kevin Walter’s work-from-home experiment lasted mere hours. On March 12, the Barclays trader was so alarmed by the turbulence flaring up in the US government bond market that he jumped in a car and made a dash from his home in Connecticut to his office in the normally crowded Times Square.

Trading conditions for US Treasuries had been poor for a while. But that Thursday — the day after Covid-19 was declared a pandemic — unnerving glitches escalated into mayhem. “It was a shock to see these distortions in the market,” says Mr Walter, co-head of global Treasury trading at the British bank.

It is hard to overstate the importance of the roughly $20tn market for US government debt, or the alarm that its mounting dysfunction in March caused. The Treasury market is the biggest, deepest and most essential bond market on the planet, a bedrock of the global financial system, and the benchmark off which almost every security in the world is priced.

Trading conditions for US Treasuries had been poor for a while, but the day after Covid-19 was declared a pandemic, unnerving glitches escalated into mayhem © Michael Nagle/Bloomberg

The wild price swings in March meant many investors struggled to offload even modest Treasury positions at sensible prices. Suddenly, broker screens were going intermittently blank and showing no pricing information for what is considered the world’s risk-free rate.

Deirdre Dunn, global co-head of rates at Citi, says it was the most dysfunctional Treasury market she has seen in her career, surpassing even the global financial crisis of 2008. Layer on top of that the practical complications of many traders working from home and the emotional stress of a pandemic, and things were getting chaotic. “The intensity of everything at that time was remarkable,” she says.

Urgent calls took place between banks and the Federal Reserve as well as the US Treasury department. Rumours of hedge funds collapsing due to imploding Treasury bets went through industry WhatsApp groups like wildfire. Some even fretted that the Treasury might face the previously unimaginable scenario of a failed auction of US government debt.

“There was a point in time when we were wondering if the bond market would really ever function again,” says Nick Maroutsos, co-head of global bonds at Janus Henderson, an investment group. “If it continued for a couple of weeks, we were thinking we were looking at doomsday.”

To avert calamity, the Fed delivered an unprecedented series of measures, surpassing even its response to contain the crisis over a decade ago. Trading conditions soon began to stabilise, volatility ebbed and before long, the central bank had stoked a historic rebound in financial markets.

Nonetheless, the events of March have cast a long shadow. Such turmoil simply shouldn’t be possible in the Treasury market, analysts say. If the financial system is a house, then Treasuries are its foundations — the safe, solid bedrock on which everything else relies. Investors can deal with a fire in the attic or leaky plumbing, but if the foundation starts creaking, it can shake the entire structure.

Policymakers must now grapple with not only what caused such a critical market to crack, but also how to address the fragility within the market that was revealed during this period of indiscriminate selling. Some experts suggest tweaks to the regulations put in place following the previous crisis, while others make the case that highly-leveraged players warrant more scrutiny.

“In a crisis like this, all the weak spots get revealed,” says Bill Dudley, former head of the New York branch of the Fed. But no one expected Treasuries to be one of them, and a thorough postmortem is now necessary, he argues. “The Fed will be doing a deep dive into this to understand what happened, and what needs to be done to prevent it from happening again.”

Bob Michele of JPMorgan Asset Management says he thought “something’s wrong here. Something broke’, on March 9 © Victor J. Blue/Bloomberg

‘In a crisis like this, all the weak spots get revealed,’ says Bill Dudley, former head of the New York branch of the Fed © Christopher Goodney/Bloomberg

‘Something broke’

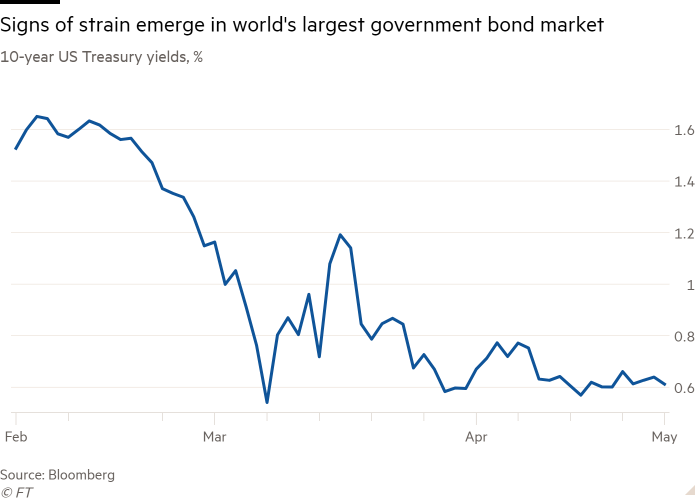

The first signs of strain emerged in early March, just days after the Fed delivered its first emergency interest rate cut since 2008. Treasury yields had been falling for weeks, a sign that investors were gearing up for an extraordinary economic shock.

But on March 9, “all hell broke loose”, says Bob Michele, chief investment officer at JPMorgan Asset Management. Oil prices cratered on a price war between Saudi Arabia and Russia, while stocks tumbled. To the surprise of many investors, so too did Treasuries.

The previous Friday, 10-year Treasury yields hovered around 0.76 per cent. That Monday, they plummeted to an all-time low of 0.31 per cent before whipsawing higher to 0.6 per cent. Yields on 30-year notes dropped from 1.28 per cent to below 0.7 per cent, before climbing again.

These may seem like modest moves compared to the wild swings often seen in stocks, but for Treasuries, it was discombobulating. “Something’s wrong here. Something broke,” Mr Michele thought to himself that day.

The core cause was a panicky “dash for cash” by companies, foreign central banks and investment funds girding themselves for torrential outflows at a time when financial hubs globally were transitioning to working from home. That meant selling what is typically easiest to sell: Treasuries.

But the panicked move to raise liquid funds was not the only reason. Compounding the volatility was an under-appreciated evolution in the Treasury market ecosystem. Over the past decade, high-speed algorithmic trading firms have become increasingly integral in matching buyers and sellers in the Treasury market, with many “primary dealers” — the club of big banks that arrange government debt sales — copying their tactics.

Electronic-style trading activity now accounts for more than 75 per cent of liquidity provision in the Treasury market, according to estimates from JPMorgan, up from just 35 per cent after the 2008 crisis.

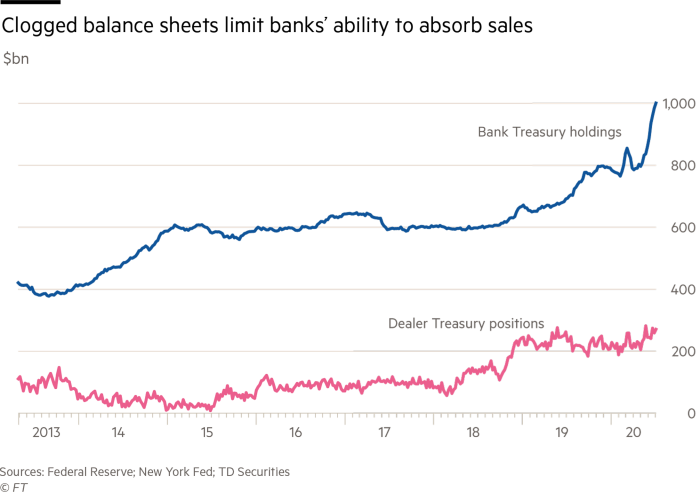

The trend has been magnified by post-2008 regulations that made it more costly for banks to store bonds on their own balance sheet and therefore less able to ensure that markets function efficiently, analysts say.

In normal times, algorithmic market-making helps to keep trading conditions smooth and ensures tiny gaps between bids and offers for even big chunks of Treasury bonds. But when volatility spikes, market-makers automatically ratchet back the size of trades they are willing to do, and pricing quotes on purchases and sales are widened to compensate for the additional risks.

Moreover, banks and dealers’ holdings of Treasuries were already elevated at the onset of the crisis. That meant they had less capacity to absorb the relentless pace of selling. As a result, the bid-offer spread for 30-year Treasuries at one point blew up to more than six times the average since the crisis, according to the New York Fed. For 10-year notes, the benchmark Treasury, it doubled.

The biggest dislocation was in “off-the-run” Treasuries, which make up the majority of outstanding Treasury debt. These are older issues of bonds that trade far less frequently and are therefore a little cheaper than more recently-issued “on-the-run” Treasuries. At some points in March, investors say, market-makers were simply not quoting prices.

At the time, some analysts and investors blamed so-called “risk parity” funds for contributing to the turmoil. These are leveraged investment funds that allocate to a wide array of assets weighted according to their volatility. In theory, this ensures a more mathematically balanced and diversified portfolio than merely allocating fixed dollar amounts to various asset classes. When Treasury volatility spiked, they had to pare their positions. But most analysts now reckon that they were only a minor factor in the chaos.

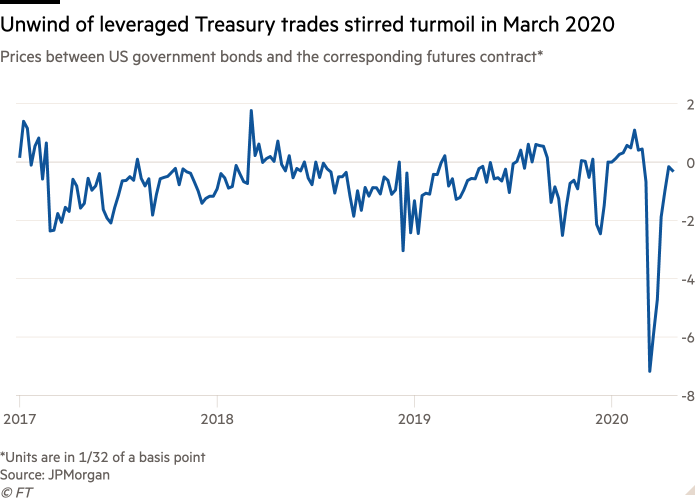

The dysfunction was instead exacerbated by the unwinding of what is known as the “basis trade”. It involves highly-leveraged market participants arbitraging the difference between Treasury futures and Treasury bonds, which are slightly cheaper than futures due to different regulatory treatment. A favourite trading strategy has been to buy cash Treasuries and sell the corresponding futures contract.

The price differential is often small, but hedge funds can juice returns by using huge amounts of leverage. The main way to do so is by swapping Treasuries for more cash in the “repo” market, one of the world’s largest hubs for short-term, collateralised loans. The extra cash can then be recycled into even bigger positions, repeating the process to further augment returns.

These trades have exploded in popularity since the financial crisis, as hedge funds — such as Capula Investment Management, Millennium Management, ExodusPoint Capital Management and Citadel — jumped into the void left by hamstrung bank trading desks.

According to the Bank for International Settlements, these “relative-value” strategies were also at the heart of the crisis that gripped the repo market last September, exacerbating a cash crunch that sent short-term borrowing costs soaring. In a recent report, the BIS called the 2019 event “a canary in the coal mine” for March’s ructions. In July, former Fed chairs Ben Bernanke and Janet Yellen also singled out the role that hedge funds played in March. Capula, Millennium, ExodusPoint and Citadel declined to comment.

When Treasury prices began sliding compared to the corresponding futures contract — as investors ditched US government debt to raise cash — the trades began racking up steep losses. Banks then demanded more collateral from hedge funds, forcing many to cut their losses and worsening the dislocations further.

Relative value players are big buyers of Treasuries, but the exact size of their basis trade exposure is unknown. One proxy is gross short futures positions for leveraged funds. According to data from the Commodity Futures Trading Commission, the main US derivatives markets regulator, the size of these positions has grown approximately eightfold since 2010, and at the start of the year it was more than $750bn.

In March and April, it dropped by about $200bn, according to Josh Younger, an interest rate strategist at JPMorgan.

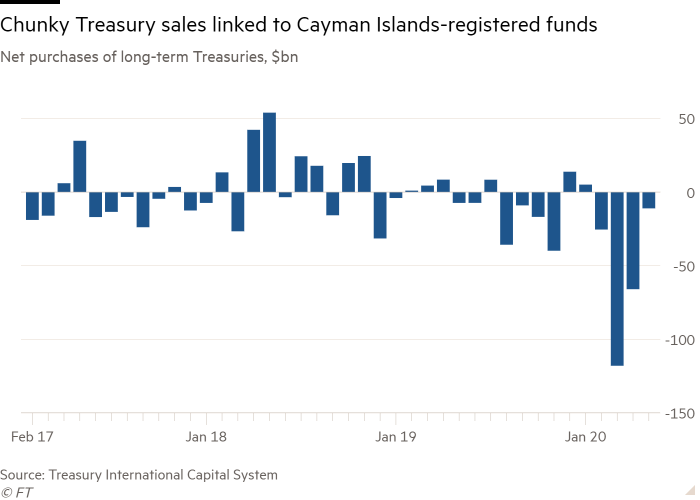

Moreover, recent transactions data from the Treasury showed that foreign investors offloaded a record roughly $300bn long-term Treasuries in March, and another $177bn in April. More than a third of March’s sales came from the Cayman Islands — a favourite domicile for hedge funds, analysts say. The following month, the low-tax jurisdiction was the largest net seller.

A continuation of this pattern could have been dire. “With the market dislocated to that extent, it raised the risk that the government couldn’t fund itself,” according to a senior hedge fund executive. “It just had to be fixed.”

Recognising the Treasury market’s mounting fragility, the Fed stepped into the fray and ramped up its liquidity injections into the repo market from March 9 onwards. Days later, it had cut rates to zero and expanded the scope and scale of securities it would buy, among other emergency measures.

When that proved insufficient the central bank pulled out all the stops on March 23, pledging unlimited asset purchases and wading into corporate debt markets. It later rolled out a facility to limit Treasury sales from foreign central banks, eased a bank capital rule and unveiled programmes to support an extensive swath of asset classes.

In taking decisive action to stabilise the Treasury market and avert a more acute crisis, the Fed has received many plaudits. But the mayhem in March is a thorny topic that will not fade as easily. It has raised uncomfortable questions about the unintended consequences of the Fed’s interventions and the underlying vulnerabilities of what is supposedly the financial system’s safest haven.

Moral hazard

One issue involves the heavily-leveraged hedge fund trades, and the de facto rescue that some say the Fed provided as these positions were unwound. “I understand why the Fed did this, but they basically bailed them out,” says Mr Dudley. “There’s definitely a moral hazard here.”

Many in the finance industry agree, questioning whether relative-value traders should be encouraged to build so much leverage given the post-crisis landscape.

“One can argue that the (activity) helps to lower interest costs for taxpayers during periods where there is no volatility, but are we comfortable with central banks having to step up in this magnitude and become liquidity providers of last resort when this levered trade blows up going forward?” asks Matthew Scott, head of the global rates, securitised assets and currency trading teams at AllianceBernstein.

Donald Trump meets oil industry executives. In early March, oil prices cratered on a price war between Saudi Arabia and Russia, while stocks tumbled © Doug Mills/Getty

A trader walks beneath a stock display board at the Dubai Stock Exchange © Giuseppe Cacace/AFP/Getty

To redress this, the BIS has recommended “full fledged stress tests” to evaluate the potential for forced selling among highly-leveraged traders and vicious feedback loops. They say monitoring should include “what if” questions that look beyond periods of market tranquility.

The March meltdown has also prompted calls to “upgrade” the Treasury market’s trading infrastructure in order to improve transparency.

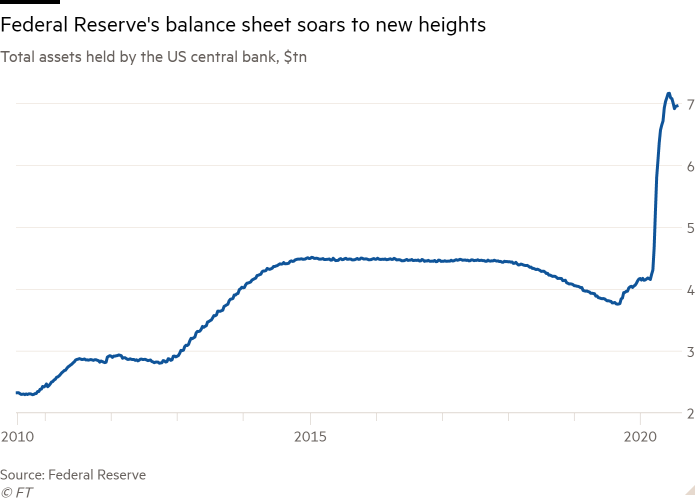

More broadly, investors fear the consequences of a world in which the Fed has the sole balance sheet flexible enough to absorb securities ditched during fire sales, especially at a time when Treasury issuance has soared to fund a record-setting deficit. In just six months, the Fed’s balance sheet has ballooned from over $4tn to $7tn.

Some advocate for the regulatory relief measures extended temporarily to banks be made permanent, enabling these entities to step in more forcefully during periods of stress. Others accept that these rules mean the Fed sometimes has to play an “activist” role, as Mr Younger puts it.

But for Peter Fisher, formerly the head of the Fed’s market desk and BlackRock’s bond investing division, now at Dartmouth’s Tuck School of Business, this fragile equilibrium will only grow more brittle as the Fed wades deeper into the fabric of financial markets.

“The big balance sheet undermines the behaviour of market liquidity and replaces it with, ‘you can do business with the Fed’,” he says. This results in a more placid trading environment, but risks more ferocious bursts of turmoil.

“The Treasury market is still the biggest and deepest bond market in the world. But compared to expectations, it clearly fell far short in March.”

You may also like

-

Marketing Nationally And Locally Simultaneously – Which Techniques Work For Both

-

Marketing A Local Business On The Border Of Two Regions

-

City-Specific YouTube Playlists And How They Can Rank In Search Engines

-

Using YouTube Playlists To Help Generate More Business

-

The thriving tech scene makes Uruguay shine during a pandemic