Covid-19 has left debilitating symptoms in many patients after the initial infection subsided. This is "Long Covid". What applies to health risks also applies to the economy. The pandemic is likely to bring not only a deep recession to the world, but also years of weakness. To counter the threat of a "long economic covid," policy makers need to avoid repeating the mistake of withdrawing support too early, as was the case after the 2008 financial crisis.

This danger is real, even if there is still great uncertainty about how the crisis will develop. Last but not least, we do not know when Covid-19 will be brought under control quickly or completely.

However, we already know a lot about the economic impact of the pandemic. We know it caused a huge global recession; that the economic costs were higher for young, unskilled, minority and working mothers; and that it severely disrupted education. We also know that "nearly 90 million people could fall below the $ 1.90 a day income threshold for extreme deprivation this year," as the IMF put it.

We know many companies have been hurt when demand for their production collapsed or they were suspended. The second waves of the disease now appearing in many economies will make this worse. As the IMF's Global Financial Stability Report shows, financial fragility is increasing in already highly indebted sectors of high-income economies as well as in emerging and developing countries.

But we also know that it could have been much worse. The world economy has benefited from the exceptional support from central banks and governments. According to the IMF Fiscal Monitor, fiscal support was "$ 11.7 billion, or nearly 12 percent of global GDP as of September 11, 2020". This is far more than the support offered after the global financial crisis.

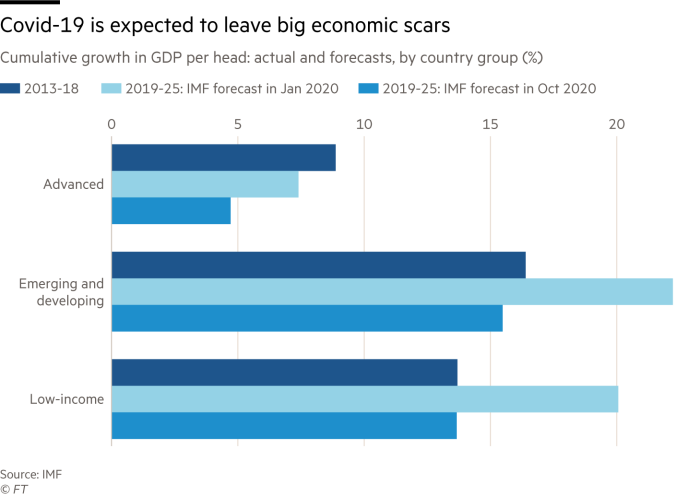

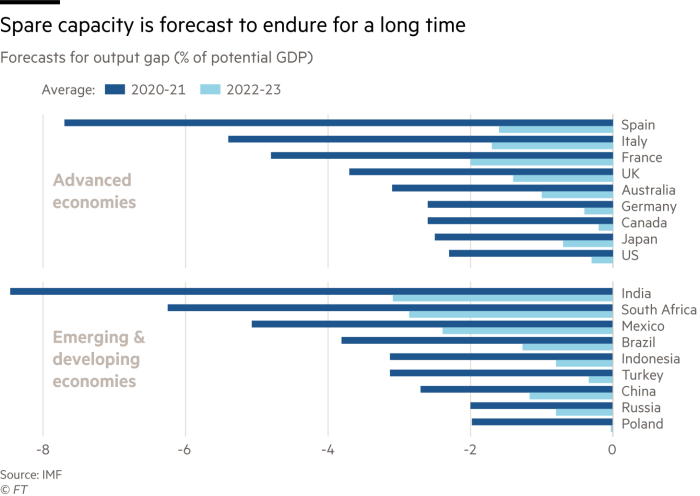

However, we know that what has already happened will leave deep scars. The longer the pandemic lasts, the bigger these scars will be. The IMF is already forecasting a large decline in economic activity in relation to potential for 2022-23. That is certain that private investments will remain cautious. Unsurprisingly, the fund is forecasting significantly lower growth in real gross domestic product per capita between 2019 and 2025 than in January.

In a crisis of this magnitude, there is only one company that can act as both an insurer and a supporter of demand. Unfortunately, the ability of governments to act varies greatly. But those with globally accepted currencies have enormous room for maneuver. You've already used it; You have to keep doing this.

Fiscal policy must play a central role as it alone can provide the targeted support needed. The central bankers knew this. The Fiscal Monitor usefully divides the required support into three phases: blocking; gradual reopening; and recovery after Covid.

During the lockdown, cash transfers, unemployment benefits, short-time work support, temporary deferral of taxes and social security benefits, and liquidity support for companies must be the responsibility.

During the reopening, support needs to be more targeted, with incentives aimed at getting people back to work. Plans should be made for greater public investment. In the meantime, support for businesses needs to be focused on those who have good prospects but are in control of dividends and executive compensation.

In the post-Covid era, the social protection systems that the pandemic has shown to be defective need reform. In the meantime, attention must be paid to active labor market policies and a sharp increase in public investment. This, the Fiscal Monitor argues, will greatly stimulate private investment. Mechanisms for accelerated debt restructuring are also needed.

It will be difficult to get all of this right, especially since the timing of the transitions between the different stages of the disease is uncertain and may not go in one direction. Policy makers need to be flexible, but not frugal.

All of this spending will add substantial public deficits and debt. The state's global budget deficit is projected to reach 12.7 percent of GDP this year. In high-income economies it will be 14.4 percent. The global government debt-to-GDP ratio is projected to increase from 83 to 100 percent of GDP between 2019 and 2022, while for high-income countries it will increase from 105 to 126 percent.

Never mind. In high-income countries, the real interest rate on long-term loans is zero or less. The central banks also credibly advocate a very simple monetary policy. Governments can afford to spend money. What they cannot afford is not to do so, to shake economies, make people feel abandoned, worsen economic scars, and economies experience sustained slower growth.

Governments have to spend. But over time, they need to shift their focus from salvation to sustainable growth. Ultimately, if taxes have to rise, they have to fall on the winners. It is a political imperative. It is right too.

We are only at the beginning. We can't know how this will end, not least because we don't know what those in power will do. We know, however, that history will judge policy-makers harshly if those who have the space do not seize the opportunity.

A long economic Covid must be prevented. This does not mean giving up efforts to fight the disease, but vice versa. It will require active, imaginative and courageous economic policies for years to come. Don't worry about what this will cost. Worry a lot more about what it will cost not to do it.

You may also like

-

Maryland Circuit Court Dismisses Derivative Complaint against Defendants Farmland Partners

-

Marketing Nationally And Locally Simultaneously – Which Techniques Work For Both

-

Marketing A Local Business On The Border Of Two Regions

-

City-Specific YouTube Playlists And How They Can Rank In Search Engines

-

Using YouTube Playlists To Help Generate More Business