An action-packed week is ahead. Elections in Germany will be crucial to the eurozone spending agenda, while Japan’s ruling party will also elect its new leader. In China, Evergrande’s effects are unlikely to get out of hand, but upcoming PMIs will tell us if they have already started infecting economic growth. There is also a ton of data releases from the major economies and a rare meeting of G4 central bank governors.

Fed says “all systems go”

This week’s Fed meeting did not disappoint. Chairman Powell essentially signaled that the tapering process will begin in November without a disaster, while the new rate forecasts showed the FOMC is now evenly divided on whether or not rates will hike next year. He also downplayed the impact of Evergrande and spillover risks on America.

Despite this restrictive message, the dollar is struggling to sustain its gains. This is probably due to a certain degree of market relief, so that Evergrande will not collapse in a disorderly manner, which has for the time being made the reserve currency shine. Someone is listening to the Fed, however, as futures markets have fully priced in the first rate hike for December 2022, which is driving government bond yields higher.

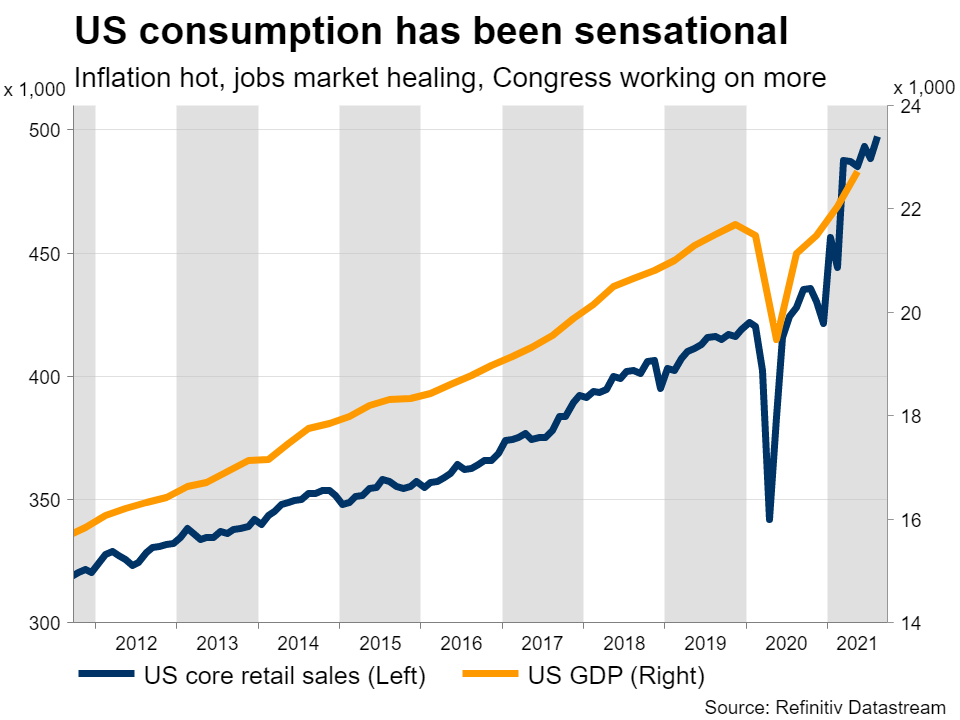

The main question now is how quickly the tapering process will be completed and whether an even earlier rate hike – around September 2022 – is possible. Indeed it could be. Inflation could stay high for a while as supply disruptions don’t get better, consumption is well above pre-crisis levels, the labor market is likely to return to full employment next year, and Congress boosted growth by approving a massive spending bill.

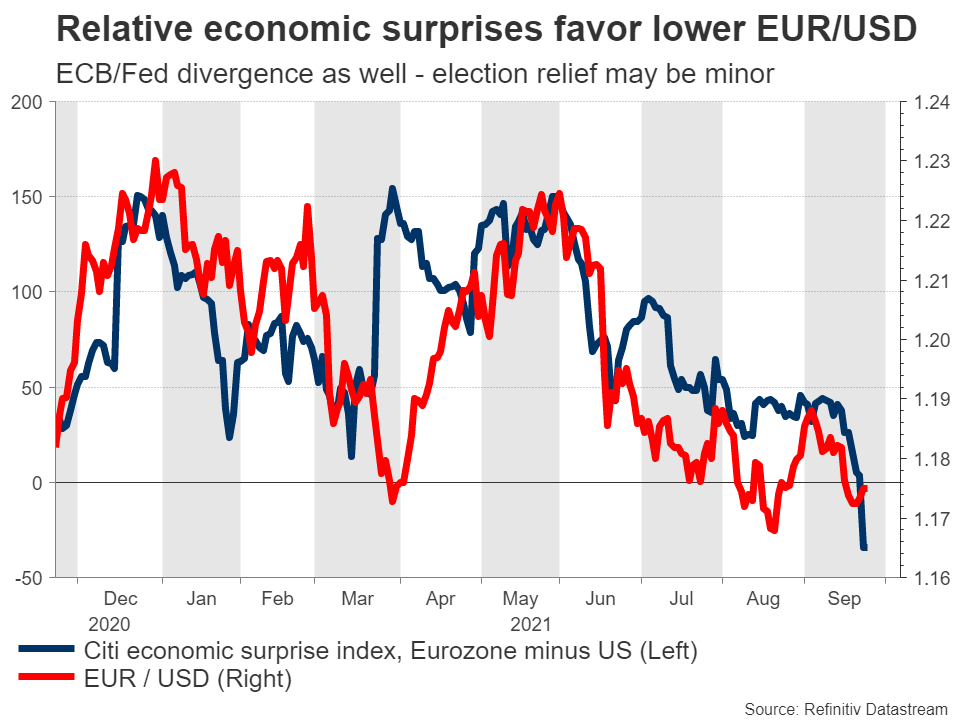

In short, the overall picture for the dollar remains quite encouraging as the Fed outnormalizes the ECB and the BoJ. As for next week, there is a deluge of US data starting with durable goods orders on Monday. On Friday, personal income and consumption figures as well as the Fed’s most popular inflation figure will be published. The main release, however, will be the ISM Manufacturing PMI for September, which gives us a taste of the next job report.

Germany is right

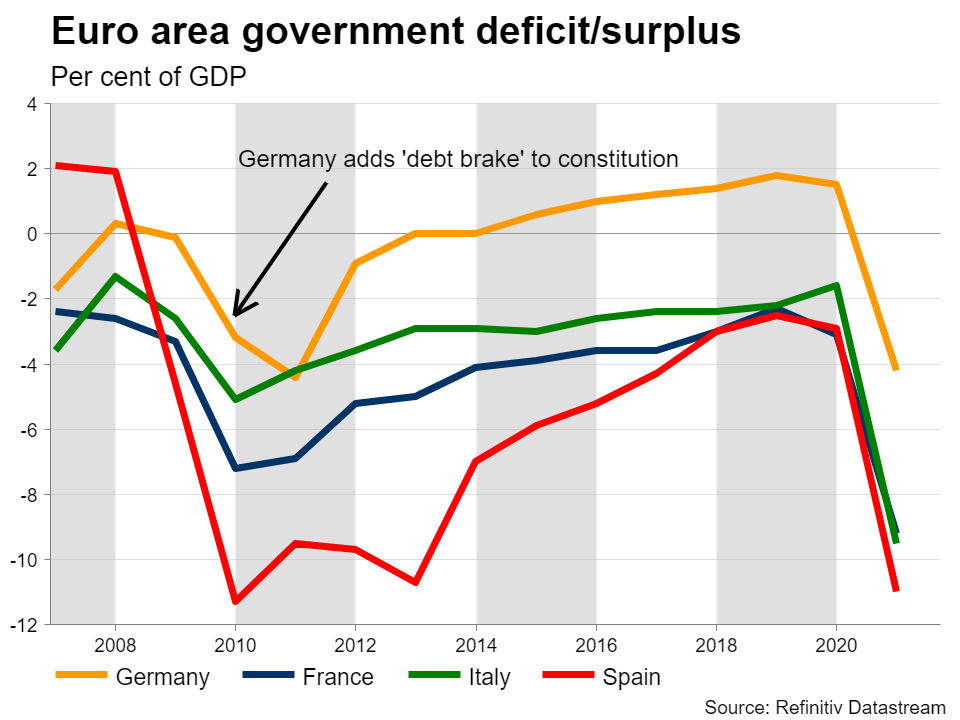

The wind of political change is blowing in Germany. Voters will vote on Sunday, in an election that could end decades of strict budgetary rules. Since it is unlikely that a single party will achieve a majority, strategic alliances must be forged.

Opinion polls are currently favoring the Social Democrats, led by Finance Minister Olaf Scholz. He led the economic fight against the pandemic, so he is considered an experienced crisis manager. In second place is Merkel’s conservative CDU, whose new chairman Armin Laschet has not really been well received by the public. The Greens are in third place and will likely be the kingmakers of this election.

The most likely outcomes are either a center-left coalition led by the Social Democrats or a center-right coalition led by the CDU. According to surveys and betting odds, the left alliance is the most likely scenario. This would allow for greater investment both domestically and at European level, so the euro could storm higher if investors realign their expectations for economic growth.

On the other hand, a coalition led by the CDU would signal a continuation of the conservative policy with less spending and a possible return to balanced budgets. Other EU countries would also come under pressure to follow suit, which would slow the recovery. This is a euro negative cocktail.

The catch is that the winning coalition will likely go undisclosed for days or even weeks while the parties negotiate. If the result is tight and the final winner is not clear, the euro’s initial reaction on Monday could be a gap lower amid the uncertainty.

After the election, there will be an ECB forum on central banks on Wednesday. We’ll be hearing from the heads of the ECB, BoJ, Fed and BoE so it should be very interesting for the forex markets. The latest inflation data from the euro zone will also be released on Friday and could reflect rising energy prices across the continent.

Japan also gets a new leader

In the land of the rising sun, the ruling party LDP will take place on Wednesday. The winner is almost guaranteed to be the next prime minister due to the majority of the party in parliament, but may not hold that position for long as there will also be a national election in the next two months.

The top three in the LDP election are Taro Kono, Fumio Kishida and Sanae Takaichi. Kono is leading the race in support of a spending package focused on increasing wages and growth. He has also asked the Bank of Japan in the past to devise an exit strategy out of cheap money so that he could replace Governor Kuroda with a less “aggressive” one when his term ends in 2023.

Kishida is more conservative. He advocates higher spending, but has historically advocated balancing the books and warned that the BoJ’s stimulus packages cannot last forever. After all, Takaichi is the exact opposite. It favors massive government spending and an ultra-loose monetary policy.

For the yen, Kono could be the best scenario given its incentives for businesses to hike wages and the prospect of a more conservative BoJ governor. Takaichi, on the other hand, would imply a continuation of “Abenomics,” which is bad news for the currency. Politics aside, the BoJ will also release its quarterly Tankan business survey on Friday.

China’s controlled demolition

Of course, the evolution of the Evergrande situation could be infinitely more important to market sentiment. At this point in time, it looks like most of the contagion will be confined to the local real estate sector rather than spilling over into the financial system. The Chinese government is reportedly working on a restructuring deal that would be effective in preventing contagion and protecting domestic investors.

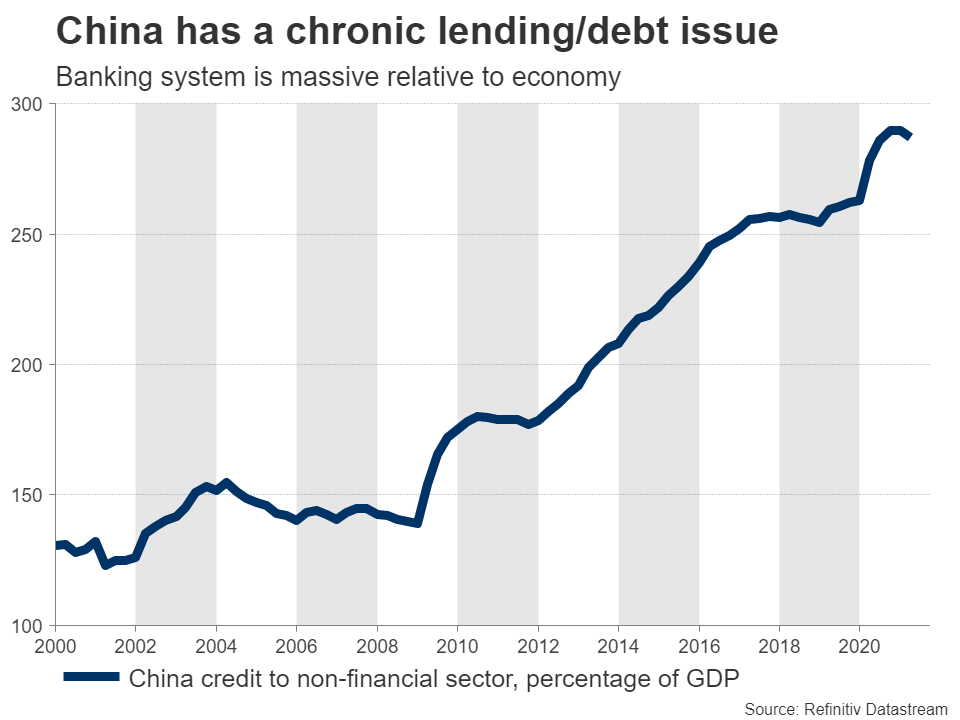

The real question is whether this is causing a massive hangover in the real estate sector, which accounts for nearly 30% of GDP. China’s economic data pulse has already slowed, so this catastrophe could further dampen growth. And the authorities cannot simply “refresh” the economy with a flood of cheap money, as they have in the past, as the banking sector is quite indebted.

Because of this, the country’s PMI business polls for September will be closely watched on Thursday. If the economy continues to lose momentum before the Evergrande debacle, this could hurt China’s sensitive currencies such as the Australian dollar.

Comments are closed.