Natural gas futures declined for the fourth straight year on Tuesday as traders considered cooling weather patterns and disruptions in US exports of liquefied natural gas (LNG). However, global demand remains robust and winter stocks are scarce, leaving the potential for supply shortages and price spikes in the coming weeks.

At a glance:

- Futures are falling for a fourth session in a row

- Forecasts lose cooling degree days

- Cash prices are falling across the country

The Nymex contract fell 18.0 cents a day in October and settled at $ 4.805 / MMBtu. November also fell 18.0 cents to $ 4.842.

NGIs Spot Gas National Avg. Down 34.0 cents to $ 4,750.

Tuesday’s futures promotion marked the second day in a row and the second time in the last seven sessions that the prompt month closed below $ 5.00. This signaled that the market had to correct downward “after a fierce but exaggerated four-week rally” that began in August and continued well into the current month, the EBW Analytics Group said.

[Business Process Optimization: Are you an NGI data subscriber? You can sync your data automatically and easily. Find out how.]

After forecasting cooler temperatures for the coming week, NatGasWeather said Tuesday that both the American and European weather models are also losing degree days for the next week. The forecasts showed “bearish weather patterns for the next 15 days”, which further dampened the excitement in the futures markets.

“Most of the US sees perfect highs from the upper 60s to the mid-80s, with coverage declining significantly in the 90s and limited to areas of California, the Southwest and South Texas,” the company said. “How long this comfortable US pattern lasts is of great interest as it will lead to much larger supplies until a more impressive cold arrives that we see opportunity for near or after October 7th at the earliest.”

NatGasWeather also noted that the US Energy Information Administration’s (EIA )’s last two storage pressures were higher than markets expected, and production had rebounded to over 91 billion cubic feet per day this week. Production had dropped to about 90 Bcf / d or less in the first half of September after Hurricane Ida wreaked havoc in the Gulf of Mexico (GOM) when it crashed ashore in Louisiana on August 29.

Additionally, Freeport LNG in Texas continued to struggle with production problems after former Hurricane Nicholas lost power last week. The Cove Point LNG terminal in Maryland also ceased operations for 20 days of maintenance on Monday. LNG feed gas volumes fell to around 9.6 Bcf on Tuesday, well below the 11 billion level.

However, the demand for US LNG is robust and volumes are expected to come back into effect after the maintenance. The reasons for this are low global gas supplies and precariously scarce conditions in Europe after a particularly long heating period on the continent last winter and a lower than usual availability of wind energy this summer.

In addition, Barclays analysts said that “falling domestic production” and “limited pipeline imports due to maintenance work and a tight gas market in Russia have limited inventory replenishment in Europe to very low levels”.

Natural gas demand was also robust in Asia, mainly due to China’s economic recovery from the pandemic. Global gas prices have risen sharply this year.

“Another severe winter could push prices up well into 2022,” said the Barclays analysts.

The International Energy Agency (IEA) warned in a statement on gas prices on Tuesday of potentially poor supply and price conditions should the coming winter in Europe turn out to be tough.

“European prices also reflect the general dynamics of the global gas market. There were severe cold spells in East Asia and North America in the first quarter of 2021. This was followed by heat waves in Asia and drought in various regions, including Brazil, ”the IEA said.

“All of these developments contributed to the upward trend in gas demand,” added the global energy watchdog. On the supply side, global LNG production was “lower than expected due to a number of unplanned outages and delays around the world and delayed maintenance from 2020”.

There is increased demand for US exports when domestic supply is below average for this time of year too. This has sometimes raised concerns about the possibility of insufficient storage for the Lower 48 should winter start early.

While storage injections have been solid for the past two weeks, underground inventory build-up has been modest for most of the summer.

Storage outlook

For the week ended September 10, EIA reported an injection of 83 billion cubic feet into natural gas storage, dwarfing estimates and pushing inventory levels to 3,006 billion cubic feet. However, the construction kept shipments below the prior-year level of 3,601 billion cubic feet and the five-year average of 3,237 billion cubic feet.

For this Thursday’s report that covered last week, NGI’s model predicted an injection of 82 Bcf. Last year, EIA saw a build of 70 Bcf for the similar week, and the five-year average is 74 Bcf.

Energy Aspects predicts a building roughly in line with historical norms. It estimated an injection of 73 billion cubic feet and cited an increase in electricity usage of nearly 3 billion cubic feet per day per week for the period that resulted in a supply gain of 0.8 billion.

“Henry Hub’s pricing appears to have been trying to curb demand from the power sector, thereby ensuring adequate storage capacity throughout the feed-in season,” said Energy Aspects. “… Our carryout level from the end of October will continue to be reduced and is now at 3.48 Tcf.”

This would be significantly below the previous year’s end value of 3.9 Tcf.

Early last week, Energy Aspects saw electricity burns of over 38 billion over a three-day period. The modeling showed “several days” near the 38 Bcf / d mark for demand in the electricity sector during the current week.

“This suggests that the gas share of the energy is still sticky, which likely reflects that some coal blocks need even higher prices to incentivize shipping, especially as they protect dwindling coal supplies into winter” said Energy Aspects.

Sinking spot prices

Physical prices also fell Tuesday, led by declines in the recently volatile west, despite hubs in the Lower 48 making losses.

Temperatures remained high in the southwest and California deserts, but forecasts called for easing in the coming days.

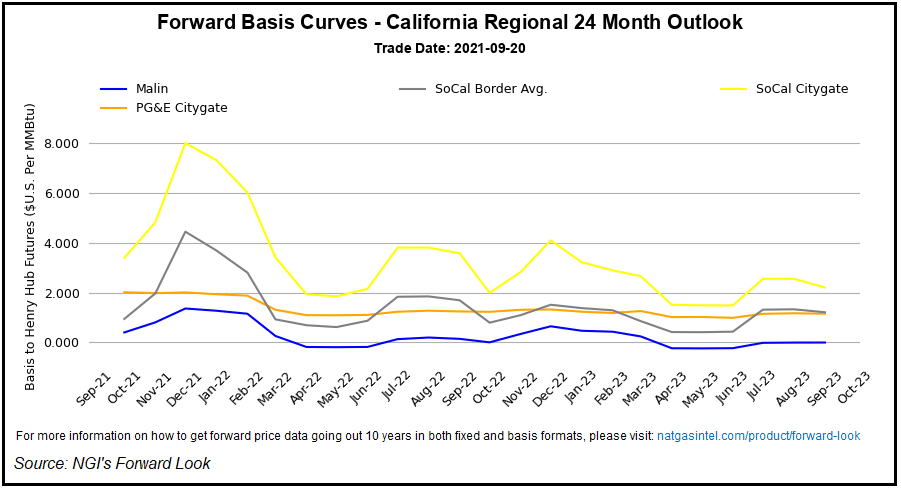

SoCal Citygate dropped $ 1,290 per day to $ 7,535 while SoCal Border Avg. lost 79.5 cents to $ 6,140 and El Paso S. Mainline / N. Baja fell $ 1.240 to $ 7.445.

Domestic demand was expected to weaken in the coming days as well, which by and large weighs on prices.

In the northeast, PNGTS fell 87.0 cents to $ 6.180, and in the southeast, Florida Gas Zone 3 fell 37.5 cents to $ 4.870. In Texas, Katy fell 35.0 cents to $ 4.745.

DTN’s weather outlook later that week showed cooler weather enveloping much of the country, including the south-central and south-east – regions crucial to late-season cooling demand. This could leave highs in much of the country in the 1960s and 1970s, minimizing both heating and cooling needs. The trend is expected to continue into the next week and the cooling degree days are forecast to decrease by more than 20.

“Falling weather-related demand and seasonal maintenance at LNG facilities could help loosen physical market support for natural gas and allow Henry Hub spot prices to decline – increasing the likelihood that Nymex futures will decline in the next seven to ten days the EBW team said.

Comments are closed.