Home buying intentions

University of Michigan

The systemic myths of “inflation” and “labor shortage” persist despite contrary data in the financial media:

- Layoffs remain at a recessive level;

- Wage growth is slowing, not accelerating;

- Bond yields fall (where’s the inflation?);

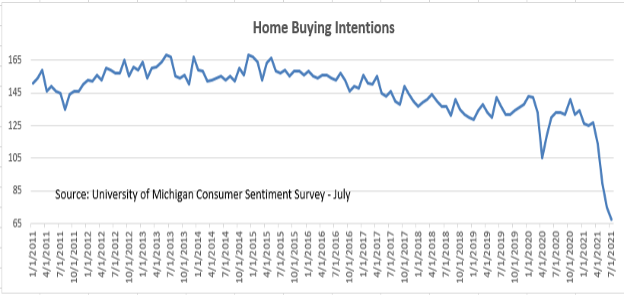

- Buying intentions for homes and cars are at a 40-year low.

inflation

The University of Michigan’s Consumer Sentiment Survey (U of M) one-year inflation expectation measure rose to 4.8% in July from 4.2% in June. But this measure correlates strongly with gasoline prices and probably with the inflation hysteria of the financial media. (The good news here is that OPEC + agreed to increase the supply.)

The more appropriate measure of inflation expectations, which has the greatest impact on inflation in the medium term and is being closely monitored by the Fed, is the measure of inflation expectations over two to five years. In the July poll by U of M that was 2.4%, less than 2.5% in June and 2.7% in March. As long as these expectations remain anchored, the Fed will not tighten (again, good news, as almost all of the Fed’s tightening cycles end in recession).

Atlanta Fed wage tracker

Atlanta Fed

Wage growth, part of the myth of financial media inflation, is limited to the low-wage sectors that still compete with federal $ 300 / week unemployment insurance (more on this below).

The Atlanta Fed wage tracker is trending DOWN and appears to be much closer to the recent lows of 3.3% of the range (May 21, September 20 and 20) at 3.4% (three-month moving average for June) to values of over 4% in the period before the 2019 pandemic (when there was no talk of inflation, let alone “systemic”). The bond market has recognized this, and while 10-year government bond yields are still somewhat volatile, as of this writing they have managed to fall from 1.54% (June 24th) to 1.28%. Obviously, bond traders don’t see any systemic or other inflation, otherwise the T-Note yield would rise, not fall!

The labor shortage

The latest weekly data (July 17) (not seasonally adjusted) shows that initial unemployment claims (ICs) (government programs) have increased by more than 23,000 to 406,000 (up from 383,000 reported last week to 392,000 corrected). In a growing economy, the normal value for this series will fluctuate around 200,000. In addition, the special Pandemic Unemployment Assistance Program (PUA) also showed an increase of + 14K (from 96,000 to 110K). These series are proxy for new layoffs. If business is doing so well, why are layoffs still at a recessive level? (In that regard, business may be good for large companies, but not so much for smaller ones.)

On July 10, Continued Unemployment Claims (CCs) were 12.6 million; 2 million was normal before the pandemic. And while this is a nice downward move from the previous week’s level of 13.8 million, all of the improvement has been focused on the states that have opted out of the federal government’s $ 300 per week unemployment insurance allowance (see below).

Continued Unemployment Rights (CCs)

Universal value advisor

The “labor shortage” seems to be limited to the low-wage sectors (leisure / hospitality). Both the NY Fed and Philly Fed recently reported that their employment sub-indices rose significantly (NY in their July poll and Philly in both June and July). In the Fed’s mid-year monetary policy report, it put the unemployment rate at 8.7% with full employment in the region of 4%. Looks like a lot of slack to us!

Once again, the data by state is compelling that $ 300 unemployment benefits is a major factor keeping service workers on the sidelines. The table shows the percentage changes in unemployment between the 15 May and the last three reporting weeks.

Percentage changes of the CCs after the deregistration date

Universal value advisor

Note the continuing downward trend in unemployment in the states that have already exited while those that haven’t lost ground in the week of July 10th. The aggregation of the data for the states that have already left the supplementary program shows a -21.7% change in unemployment compared to the -2.5% change over the two-month period for the opt-ins.

Yes, you read that right. The week of July 3rd had shown the opt-ins with a delayed but healthy change in unemployment of -7.7%. But CA showed a huge surge in the week of July 10th. If CA is removed from the mix, the rest of the opt-ins show up with a respectable 11.7% unemployment rate since May; but still only about half as fast as the opt-outs.

In mid-July, the national polling institute Morning Consult quoted the results of its survey from the beginning of June as follows:

“Forty-five percent of those who turned down a job offer cited the generosity of UI services as the main reason they didn’t take the job offer …”

We didn’t see any general coverage of this survey!

We expect the opt-in states to catch up in August and (especially) September. By mid-October, the signs “Help wanted” should be less ubiquitous.

Unintended consequences

There are a couple of unintended consequences of the state supplementary unemployment program:

- Its presence has led to upward wage increases in the sectors that pay the lowest (minimum) wages. Such sectors do not make up a large percentage of total employment. Perhaps that is why the Atlanta Fed’s wage tracker is behaving as described above. Politicians appear to have stumbled upon the boom in the low wage sector caused by the supplementary program; perhaps this method will be used in the future to raise the minimum wage.

- The service sectors have now developed strategies to address the shortage of low-wage workers. For example, automated orders in restaurants. In the hotel industry, some chains offer lower prices for stays of several days if the customer does not opt for daily room cleaning / room cleaning. This reduces the hotel’s need for cleaning staff with lower wages. A long-term consequence of the additional unemployment program is that the highly employment-intensive service industries may not return to their pre-pandemic employment levels as quickly. With the Fed underselling its employment mandate for this cycle, such a development could keep the Fed on the sidelines longer than markets are currently anticipating.

While the program may have boosted entry-level wages in some service industries, there may be fewer long-term employment opportunities in this area. At best a mixed bag!

Other dates

We have commented on an economy that is showing slowing characteristics on several blogs. The first GDP figures for the second quarter will be released on Friday (July 30th). Over the course of the second quarter, both the NY and Atlanta regional central banks scaled back their GDP estimates as it became clear that the reopening acceleration wore off as the second quarter progressed. Indeed, June looks very soft.

Purchase intentions

Both new and existing home sales declined over the course of the quarter (to blame for the high prices!). In addition, new car sales were weak (to blame for semiconductor shortages), as was retail sales of Real (adjusted for inflation) (free money slowed). Non-residential construction and the manufacturing of durable goods also slowed over the quarter. The latest U of M Consumer Sentiment Survey ranks both residential property and vehicle purchase intentions (leading indicators) 40 year lows (see diagrams above and below).

Vehicle purchase intentions

University of Michigan

Regardless of the reasons for the decline in these intentions, there will be a dramatic impact on economic growth (and likely prices) in the second half of the year. Perhaps the inflation narrative will die in the next few quarters.

casing

Housing starts increased dramatically in June (all in the West and South; housing starts decreased in the Northeast and Midwest). This caused the price of timber in the raw material mines to reverse its rapid decline (from $ 1,686 / 1000 feet on the 6th. On the other hand, permits, a better barometer of future activity, fell -5.1% m / m (June ), are now down for three consecutive months and for four of the last five months The consensus estimate for permits was up nearly 100,000 units, leading us to believe that the softness ahead is not yet included in the price.

Delta variant

We don’t seem quite out of the woods yet when it comes to the pandemic. The more contagious Delta variant has significantly increased the number of new infections and hospital admissions, especially among the less vaccinated population groups. While it doesn’t appear that business lockdowns are imminent or even considered (maybe a lesson learned!), Some political jurisdictions (Los Angeles, for example) have reintroduced masking requirements. But even without corporate mandates, it is inevitable that growing concerns about the spread of infection will negatively impact economic activity, likely first service consumption when consumers sit down again.

Conclusions

- Inflation expectations remain well anchored despite rising gasoline, used car and some service prices. The Fed pays particular attention to such expectations.

- Wages rise in the range of 3%; that’s a 4% + decrease in 2019 (pre-pandemic) when inflation was not mentioned.

- The weekly data continues to show that layoffs are still at recessive levels. And there is no doubt that the federal unemployment insurance allowance is a major factor in the “labor shortage” saga.

- The signs of intent to buy home ownership and vehicles (leading indicators) are at 40-year lows. Perhaps that’s why building permits have dropped lately.

- The Delta variant of Covid-19 is another unknown risk. And it’s not positive.

From a holistic point of view, the data point to a second half of the year in which economic growth will be slower than is currently factored into the financial markets.

(Joshua Barone contributed to this blog.)

Comments are closed.