Diego Thomazini/iStock via Getty Images

Written by Nick Ackerman. This article was originally published on March 16, 2022 for members of Cash Builder Opportunities.

Following their recent declines, JPMorgan (NYSE:JPM) and Black Rock (NYSE: BLACK) look like a lot better bargains. At the time of writing, BLK is down ~25% from its 52-week high – which is also its all-time high. JPM has fared slightly better, down around 20.5% as of March 16, 2022. The 52-week high is also the all-time high for JPM stock. That’s not their only selling point, however, as future earnings and dividend growth make them attractive prospects.

The entire market had a pretty rough first quarter of 2022. That certainly didn’t help the share price of these two companies. Geopolitical risks as global companies and higher expected spending may hurt these two stocks. Inflation is rampant and while that would mean higher interest rates, which should benefit JPM, those higher expenses are likely to come in the form of higher labor costs.

An indirect impact for the BLK with higher interest rates could be if they are pushed too far, which could mean a rapid US economy slowdown. A recession or even a drop in assets for BLK means reduced fees as assets under management fall. This adds to an already highly competitive space where fee reductions for their ETFs are a regular occurrence. Not to mention that they are also a big employer with over 18,000 employees. If they want to fill vacancies, they also need to be competitive when it comes to pay.

However, that’s all the bad news out of the way. What makes these names interesting are these declines and that they’re among the largest companies in the world with rock-solid balance sheets. More specifically, BLK is the largest wealth manager in the world, making it the most significant player in its field. This has resulted in steady dividend growth for shareholders over the years.

When inflation is elevated, exposure to financial stocks such as banks and even money managers can be a natural hedge. Their growing dividends were more than enough to outpace the pace of inflation. This means that an income investor in these two companies increases their purchasing power along the way.

YCharts

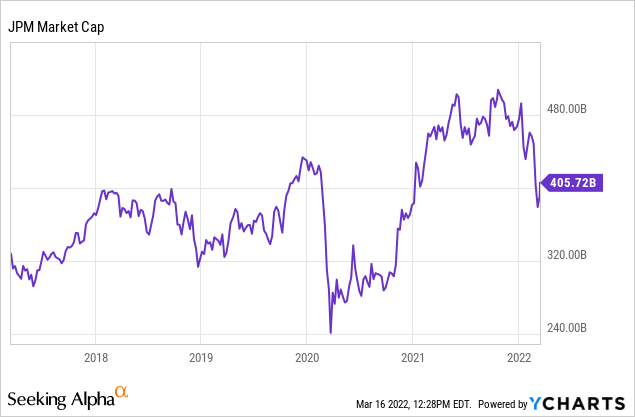

JPMorgan Chase & Co (JPM)

JPM is a huge bank with a market cap of over $405 billion. Considering the recent drop in the stock price, a lot of it is down as well.

YCharts

These declines have caused the stock to trade around where it was before the COVID-induced sell-off before March 2020. Considering that EPS was $15.36 in 2021 and $10.72 in 2019. A significant jump for this was the release of credit reserves, which meant lower earnings for 2020. Revenue increased as this also hit a record and they reported a solid ROTCE.

Looking at full year results on page 3, the company reported net income of $48.3 billion, earnings per share of $15.36 and record sales of $125.3 billion. We achieved a return on tangible share capital of 23%, or 18% without the liquidation of reserves.

Analysts are estimating that earnings for 2022 will fall significantly from current levels. Consensus per share is $11.13, which would still mean growth from 2019 onwards. A lot can happen after that, but analysts expect a fairly healthy pace of growth in 2023 and 2024. They don’t get credit for the growth over the past two years. Not to mention that they’ve beaten 13-quarter EPS expectations over the last 16 quarters. Given the consensus EPS, this would bring the expected P/E ratio for JPM to around 12.36.

They expect credit growth to contribute to strong net interest income in 2022.

JPMorgan NII Expectations (JPMorgan)

We don’t have to wait too long to see how things look as they are expected to announce their first quarter results on April 13, 2022.

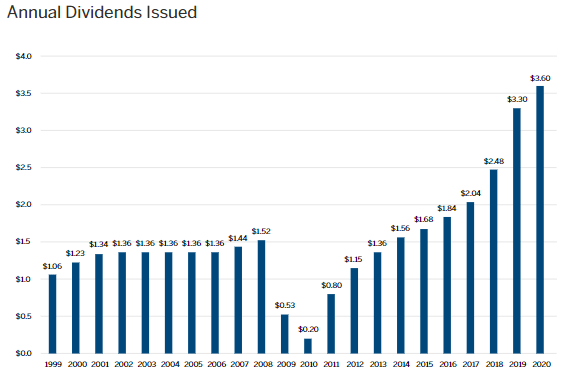

At the current price, the share yields an attractive 3.02%. They hadn’t voluntarily frozen their dividend until 2020, but instead had 11 years of consistent dividend growth since 2010. Despite the freeze, the annual amount actually paid out grew year-on-year.

As we all know, 2008/09 was incredibly tough for the financial markets. So it’s not too surprising that we would see a massive collapse of JPM’s payouts at the time.

JPMorgan Dividend History (JPMorgan)

They ended up paying $3.70 in dividends for 2021. Even if they left the dividend flat this year, it would still amount to $4 in dividends based on the $1 paid over the past two quarters. This yields a 10-year CAGR of 14.28% and a 3-year CAGR of 11.79%, according to Seeking Alpha.

BlackRock (BLK)

With their most recent earnings report, BLK hit a record high in assets under management with over $10 trillion in total assets under management. The largest of these was in the stock ETF space. That puts them well ahead of the second-biggest asset manager, Vanguard, with $8.2 trillion in assets under management. This will certainly be an interesting metric when they report their earnings in April.

With the stock hitting an all-time high and the general uncertainty surrounding the market in general, it makes sense that stocks have fallen quite steeply of late. I believe this opens up an excellent opportunity to buy shares at a much lower price than just a few months ago. For me, as a long-term oriented investor, that is easier to say. I have no doubt that the current headwinds could keep BLK stock under pressure — and so are JPM.

Unlike JPM, BLK shares are still well above pre-COVID highs. In fact, their recovery was significantly faster than JPM’s. Of course, this has to do with the respective industry – both are active in the financial sector, but the actual underlying business is very different. Below you can see the last 3 years.

YCharts

The higher earnings for BLK weren’t just an increase in value. They’ve also received some massive inflows. For 2021, they found they had total net inflows of $540 billion. This contributed to 20% higher revenue for the year and a 20% increase in diluted earnings per share. The EPS of 2020 was $33.82 and in 2021 it was $39.18. For 2022, analysts expect BLK to see earnings per share of $41.40.

Again, the number of hits in the last 16 quarters they’ve reported is 14. They’re also having a pretty hot streak; They haven’t missed a quarterly EPS estimate since June 2019.

BLK’s dividend history has been a bit more consistent compared to JPM. They go back to 12 years of dividend growth. They froze their dividend for several quarters between 2008 and 2009. That led to a lack of annual increases, but it also didn’t cut its dividend during this period.

BLK Dividend History (BlackRock)

The CAGR for BLK has been weaker compared to JPM over the past 10 years, standing at 11.87%. In the most recent 3-year period, however, it is at a similar 11.56%. This is still well above current inflation levels and the previous surge has translated into a massive 18.2% increase.

They’ve also been pretty consistent in their share buybacks over the years. That also helps that EPS number.

YCharts

Conclusion

JPM and BLK are both solid names in the financial sector. Although both operate in the financial sector, their underlying businesses are very different. At the same time, given the recent market declines, I believe these two names represent attractive entry points for long-term investors. This is given that near-term uncertainty may remain, putting pressure on these stocks.

Soaring dividends that beat inflation are a big selling point for a longer-term income investor. JPM may have cut back in 2008/09 but has been growing fairly consistently since then. BLK survived by having to freeze its dividend during that time and has grown steadily ever since.

Comments are closed.