da-kuk/E+ via Getty Images

The best portfolio is one in which all assets have the same level of risk. Using equal risk eliminates the need to decide which asset will outperform the others. It also maximizes diversification.

To create this balanced portfolio, we need to measure the risk of each asset. For stock and futures traders, this is done differently:

- Stock traders use the annualized volatility preferred by financial analysts

- Futures trades use volatility parity based on average true range, which is considered the best measure for many applications

I’m going to show how to calculate these two methods and then apply them to a portfolio of stocks or futures. From this we can see how many cryptocurrencies need to be traded in order to have a risk-balanced portfolio.

Add cryptocurrencies

Most cryptocurrencies (“cryptos”) do not have a long trading history, so for stocks we will only look at the last six years. We will compare the volatility of cryptos and crypto exchanges to see how to balance them when adding them to a portfolio.

Futures have a much shorter history, but we will see how the volatility (hence the risk) of Bitcoin (BTC-USD) and Ethereum (ETH-USD) futures contracts compares to futures for the S&P 500 (SPY) and Nasdaq (QQQ).

We know from watching crypto price movements that they are more volatile than the average stock or stock index, so we expect to need fewer stocks or contracts to have the same risk in our portfolio.

Conspicuous volatility

Figure 1 shows the price history of SPY and QQQ from 2017 and Figure 2 shows the price history of BTC-USD for the same period, both adjusted to 100 on January 4th, 2016. SPY gains 150% to a NAV of 250, QQQ gains 250% to 350 and BTC gains 44,900% to around 45,000. Quite a difference.

Figure 1. Price history of SPY and QQQ from 2016. (Data source: CSI)

Figure 1. Price history of SPY and QQQ from 2016 (Data source: CSI)

Figure 2. 2017 BTC-USD with current volatility. (Data source: CSI)

Figure 2. 2017 BTC-USD with current volatility. (Data source: CSI)

BTC-USD is clearly more volatile. But the chart can be deceiving because daily ranges widen when prices are higher, but not on a percentage basis. To show this, we plot BTC-USD prices on a semi-logarithmic scale, where the price is on a logarithmic scale (in percent), but the timescale remains the same. Figure 3 shows that the price fluctuations are more even and percentage smaller at the higher prices.

Figure 3. BTC-USD plotted on a semi-logarithmic scale. (Data source: CSI)

Figure 3. BTC-USD plotted on a semi-logarithmic scale. (Data source: CSI)

Seeing the percentage changes is important to understand the final portfolio allocation. They may not look as extreme as you might initially expect.

stock volatility

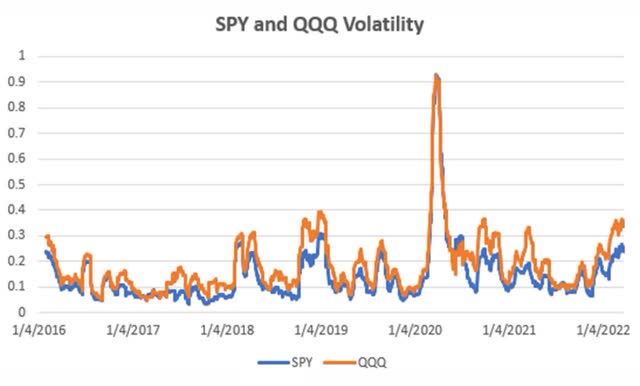

When trading cryptos, volatility means risk and cryptos are very volatile as you saw in Figure 2. We will use the average annualized volatility of SPY and QQQ as a benchmark and assume many investors have a combination of regular and technology stocks in their portfolios. Figure 4 shows that QQQ is more volatile than SPY, but both have similar patterns. The average volatility of the combined SPY-QQQ portfolio is 0.163 or 16.3%.

Figure 4. SPY and QQQ 20-day annualized volatility. (Data source: CSI)

Figure 4. SPY and QQQ 20-day annualized volatility. (Data source: CSI)

Annualized volatility

For stocks, we use 20-day annualized volatility (“AVOL”). This is how financial analysts calculate risk and VIX volatility is calculated.

The annualized volatility calculation is the standard deviation of returns over the last 20 days multiplied by the square root of 252. In Excel, that would be

AVOL = STDEV(C3:C22)*SQRT(252)

where column C contains the daily price returns, Close(n)/Close(n-1) – 1 and the square root of 252 converts the daily values to annualized.

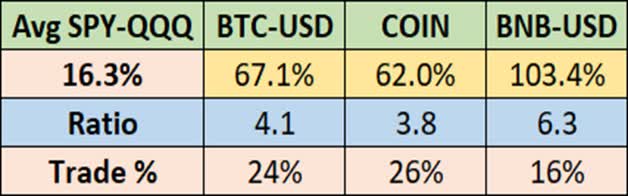

If AVOL for the SPY-QQQ combo is 16% and BTC-USD is 67.1%, then dividing 16 by 67 is 23.9%. You would be trading only $2,300 worth of BTC-USD for every $10,000 of your SPY-QQQ position. About a quarter of the value.

crypto exchanges

Stocks have both cryptocurrencies and crypto exchanges that can be traded. The most active exchange is Binance (BNB-USD), with Coinbase (COIN) gaining popularity. Using the same volatility measure, Figure 5 shows the 6-year history of volatility.

Figure 5. Crypto exchange volatility. (Data source: CSI)

compare volatility

Finding the right balance of cryptos in your portfolio will reduce risk. Let’s look at the comparable position size you would get if you combined a SPY-QQQ portfolio with either BTC-USD or a crypto exchange. Figure 6 shows that the combined SPY-QQQ has a volatility of 16.3%, much lower than any of the crypto-related markets.

If we reverse the ratio, we find that for every $10,000 invested in SPY-QQQ, we should invest 24% of that, or $2,400, in BTC-USD. Likewise, we would invest 26% in COIN and 16% in BNB-USD.

Figure 6. Relative volatility of BTC-USD, COIN and BNB-USD compared to an average of SPY and QQQ. (Data source: CSI)

To prove that these position sizes work, we calculated the returns of the four markets in Figure 7 from early 2021. We will hold $100,000 SPY, $24,000 BTC-USD, $26,000 COIN and $16,000 BNB-USD. Position sizes are determined on the first trading day. BNB-USD has outperformed the other markets and is showing on the correct scale. However, it had a similar pattern.

Figure 7. Example equity market returns using volatility-adjusted position sizes. (Data source: CSI)

futures markets

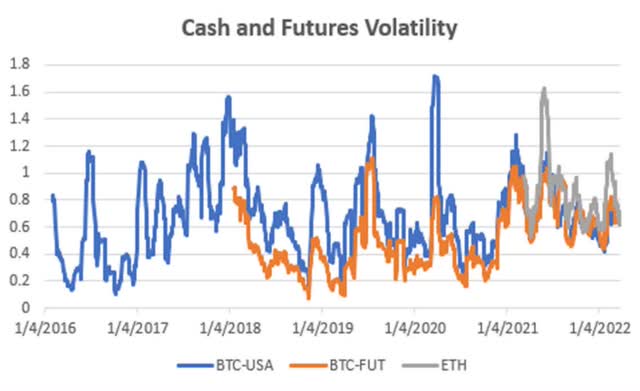

Now let’s look at the volatility of BTC-USD (stocks) and the two futures markets BTC and Ethereum (ETH). Figure 8 shows that BTC-USD has been the most volatile averaging 67%, but Ethereum, which has only a short dataset, has shown higher volatility of 84%. BTC futures have been less volatile as seen during the 2019 and 2020 spikes. BTC futures have an average volatility of 50%.

Figure 8. Bitcoin volatility compared to Bitcoin and Ethereum futures markets. (Data source: CSI)

We cannot use the annualized volatility calculation for futures as the data is back adjusted. The prices shown are not the current prices; hence the returns would be wrong. Instead, we use the average true range, similar to the daily high-low range, to define volatility.

volatility parity

Volatility parity is a more accurate measure of risk because it uses the high and low prices, while annualized volatility uses only the closing prices. It is commonly used for sizing futures positions. Its calculation is

VP = allocation / (20-day ATR x contract size for futures)

If you have 10 markets in your portfolio, divide your equity by 10 to get the allocation and divide the allocation by the average true range (“ATR”) times the contract size. The size is 5 for BTC futures, 50 for Ethereum, 25 for the S&P and 20 for Nasdaq.

To get the average true range, you need to calculate the true range, which is the daily high-low range extended to the previous close price when there is an unfilled gap. If columns C, D, and E contain the high, low, and close prices, then

True range (“TR”) F3 = MAX(C3-D3, C3-E2, E2-D3)

And the 20-day moving average of the true range is

ATR = AVERAGE (F22:F3)

After that, we get the values shown in Figure 9. For every 10 contracts of S&P futures, we would trade 2.75 contracts of NQ, 1 of BTC and 1.25 of ETH.

Figure 9. Futures relative volatility using volatility parity. (Data source: CSI)

Checking volatility parity

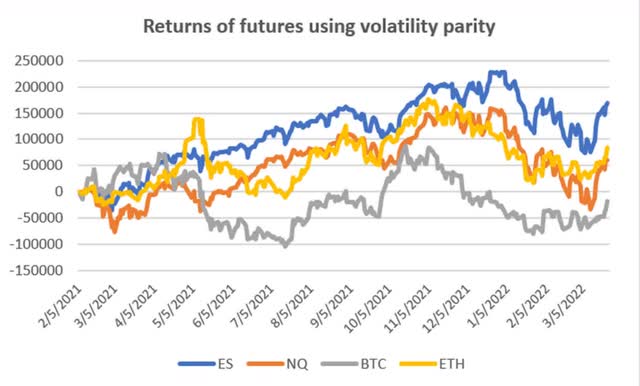

Again, we will verify our results by graphing the returns of these futures markets using position size determined by volatility parity. Figure 10 shows these results. All four markets exhibit similar patterns and volatility.

Figure 10. Futures market returns using volatility parity. (Data source: CSI)

Summary

If you trade a market with more risk than the other markets in your portfolio, that market needs to generate more return than the others; Otherwise, you’re just adding risk with no reward. Equal risk maximizes diversification.

Use annualized volatility for stocks and volatility parity for futures when calculating position size. Be sure to scale your positions to reflect volatility.

Comments are closed.