uschools/E+ via Getty Images

The Federal Reserve is curbing its purchases of securities purchased outright to add to its portfolio.

From banking week ending November 24 (the last banking week of November) through banking week ending December 29 (the last banking week of December), the Federal Reserve added just $79.1 billion in securities to its portfolio that were purchased outright.

From December 29, 2021 to January 12, 2022, the Federal Reserve just added $23.5 billion to its securities portfolio.

So the tapering process has actually started.

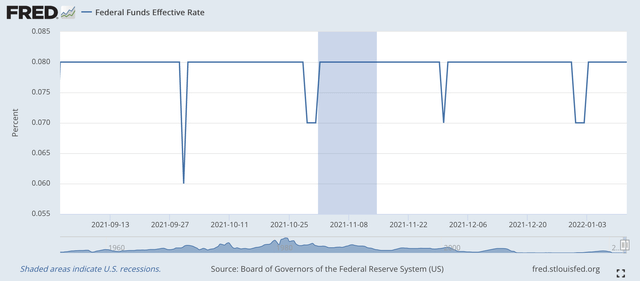

The effective federal funds rate remained at 0.08 percent through Jan. 12.

Note, however, that in order for the federal funds rate to remain at 0.08 percent, the Federal Reserve bought $66.4 billion worth of securities from the Fed.

Overall, over $120.0 billion in reserves were withdrawn from the commercial banking system in the most recent banking week, and overall commercial bank reserve balances held at Federal Reserve banks declined by nearly $100.0 billion.

That said, the Federal Reserve has started scaling back its monthly purchases, but at the same time, more than $100.0 billion in reserves were removed from the banking system and the effective federal funds rate remained at 0.08 percent for the week.

The Fed’s dilemma

Yes, the Federal Reserve has begun to reduce its monthly purchases of out-of-pocket securities, but over the past five months the Federal Reserve has had to sell securities (via the repo market) to bring the effective federal funds rate to 0.08 hold percent.

The fact that the effective federal funds rate has been so stable since September 1, 2021 reassures me that the Fed has maneuvered its portfolio of securities to keep the federal funds rate positive and constant.

Effective Federal Funds Rate

Federal Reserve Bank of St Louis

Note, however, that the Fed has purchased nearly $500.0 billion worth of securities since banking week ended September 1, 2021.

During the same period, the Fed saw its reverse repurchase operations increase by about $490.0 billion.

Indeed, what the Fed has added to its portfolio of securities through outright purchases, it has sold a similar amount under agreements to buy back the securities.

As the US Treasury increased its deposits with the Federal Reserve by over $210.0 billion during this period, the reserve balances held by commercial banks with the Federal Reserve banks actually declined.

The actual amount of these reserve balances, a proxy for excess reserves in the banking system, approached $280.0 billion.

That said, the Fed has overseen an approximately $280.0 billion drop in excess reserves in the commercial banking system since September 1, 2021.

This kept the effective federal funds rate in positive territory at 0.08 percent.

But what does that mean in terms of what Fed officials are saying now about ending tapering and raising its interest rate three or four times in 2022?

That’s the dilemma facing Federal Reserve officials right now.

From March

Federal Reserve officials have now put the tapering on record to end by March 2022.

It is also known from Federal Reserve officials that the Fed will raise interest rates three times, maybe even four times, in 2022.

This week, Fed Chair Jerome Powell, who is up for re-election as Fed Chair, and Lael Brainard, who has been nominated for Fed Vice Chair, testified before the US Congress.

Both presented a strong argument that the Fed will fight inflation and that this will be the main focus of Federal Reserve action in the near future.

But that’s as far as they went.

The financial markets have adjusted to the fact that the Fed will end its tapering and will soon start raising interest rates.

Interest rates have started to rise.

Since the end of November 2021, the yield on the 2-year US Treasury has increased from around 0.55 percent to around 0.90 percent.

The yield on the 10-year US Treasury bond has risen from 1.35 percent to 1.75 percent.

There is a broad move in the financial markets to bring yields back into more normal territory.

I’ve hinted that the yield on the 10-year bond could climb to around 2.50 percent by the end of the year.

I also indicated that many of the negative interest rates we have seen around the world, such as the German 10-year Bund yield, would move into positive territory in the near future.

New information emerging and reported in the Financial Times supports this claim.

“Pandemic-era monetary policy unwinding has pushed the global level of negative-yielding debt to $10.0 trillion for the first time since April 2020.”

At the end of 2020, the “value of sub-zero yield debt increased to $18.4 trillion.”

“A sell-off in US government bonds that began in December has played a large role in the globally dwindling price of negative debt.”

“Negative-yielding bonds now make up about 18 percent of the Bloomberg Global Aggregate Bond Index, down from 30 percent a year ago.”

So how will the Fed deal with this situation to support its interest rate?

Should the Fed start selling securities immediately and remove them from its balance sheet? And what about the $1.862 trillion in reverse repurchase agreements the Fed now has on its balance sheet?

How will the Fed fight inflation?

What will the Fed do?

The Fed has not yet come forward to define what it will do in the near future.

One problem I think they face is using reverse repos to keep the Fed interest rate in positive territory.

Fed officials haven’t talked about it at all, even though those balances have hovered in excess of $1.8 trillion.

All we heard was the $120.0 billion in securities the Fed bought outright each month.

But the Fed’s tapering actually began in the summer of 2021, when you “net” the use of reverse repos against outright purchases.

The Fed kept interest rates in positive territory throughout 2021-2022. In fact, this raised their policy rate against market forces.

So how do I move into the future?

How do we get more transparency from Federal Reserve officials?

We are certainly breaking new ground.

And Federal Reserve officials are busy.

Did the three people President Biden just appointed to the Fed Board of Governors know what they were getting themselves into?

Comments are closed.