New Zealand’s third quarter CPI inflation reading will headline Monday at 21:45 GMT. Estimates suggest consumer price growth has slowed, although unlike its Australian peer, the RBNZ has thrown cold water on rolling back plans for aggressive rate hikes. Still, some volatility in the Kiwi cannot be ruled out should any surprises spark further debate on the size of the next rate hike.

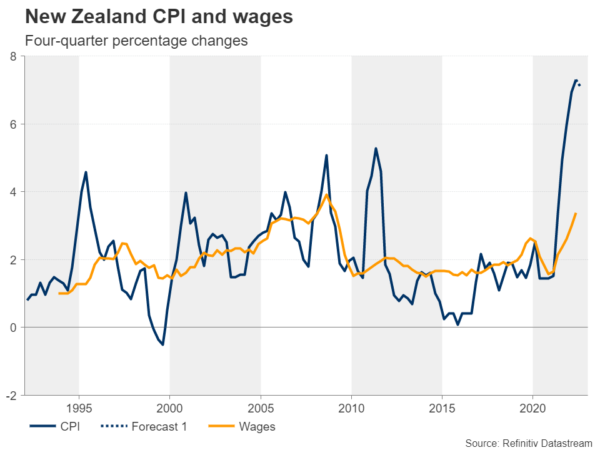

New Zealand inflation is slowing but remains in an uncomfortable zone

After beating forecasts of rising 7.3% yoy, the fastest in three decades, inflation in New Zealand is expected to have eased significantly to 6.7% in the three months to September. The quarterly change is also estimated lower at 1.6% q/q from previously 1.7% and 1.9%.

Such a result would still be well above the RBNZ’s 1-3% price target after eight consecutive rate hikes, prompting additional tightening measures. Minutes from the September meeting showed that policymakers even discussed the possibility of a bolder 75 basis point rate hike before agreeing on a half-point hike. This scenario could come back into play if inflation comes in above expectations. Also, the relatively low estimates leave room for a positive surprise.

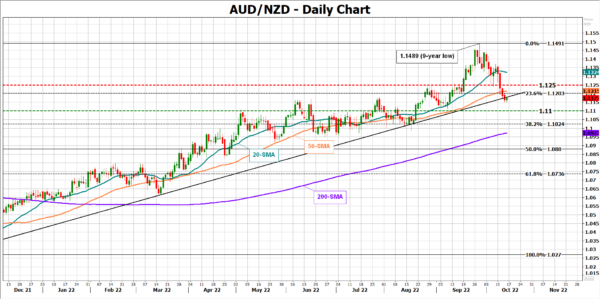

As a result, the Kiwi could extend its rebound against its Australian cousin, which turned south after the RBA surprisingly moved to a more moderate 25 basis point rate hike earlier this month. For now, futures markets are certain for a softer rate hike of 50 basis points to 4.0% in November.

The New Zealand economy is vulnerable

The lifting of travel and other Covid restrictions averted a tech recession in the June quarter, and the deputy prime minister offered some relief after saying the economy can avoid a recession even amid a global slowdown. He also forecasts a return to a current account surplus in 2025.

In reality, however, the economic picture is still sluggish. The trade deficit widened sharply to the largest ever, despite the Kiwi’s depreciation in August. Its biggest trading partner China also continues to face numerous challenges, from business closures due to zero-Covid restrictions, to a housing bubble and a renewed escalation in tensions with the US.

Internally, despite its recent surge, wage growth remains more than halfway below inflation, and higher borrowing costs will inevitably lead to more mortgage pain as household debt remains among the highest in the world. The housing market continued to cool in September, with below-average sales and lower prices, according to Westpac’s latest report. Consumer sentiment also deteriorated near record lows. However, signs of weakening demand, driving down high prices, may be what the central bank wants to achieve after all.

RBNZ remains hawkish; AUD/NZD outlook

All in all, the RBNZ appears to be following in the Fed’s footsteps, making the RBA’s unexpected pivot seem premature for now. Perhaps the data could reignite the debate between a 50 basis point rate hike and 75 basis point rate hike if inflation hits stronger than investors expected. In that case Aussie/Kiwi could slide towards 1.1100 psychological level. Still lower, the region around 1.1025, coinciding with the 38.2% Fibonacci retracement of the uptrend from 1.0276 to 1.1489, could attract attention next. On stronger declines, the 200-day simple moving average (SMA) could also come into view.

Should inflation miss forecasts, traders will likely remain confident that the rate will rise by 50 basis points, likely keeping the Kiwi steady. From a technical perspective, Aussie/Kiwi needs a break above the nearby 1.1200-1.1250 restrictive area to hit the 20-day SMA at 1.1324.

Comments are closed.