The prices for 2025, 2026 and 2027 provide insight into what lies ahead for consumers.

The biggest energy/climate policy news of the year so far is Biden's decision to suspend permits for liquefied natural gas (LNG) export facilities. Regardless of your opinion on the decision, the economic, environmental and political implications of the move are fascinating and complicated, and this story will likely remain in the news for some time.

For today's blog post, I want to look at futures price data to see how it was affected by the decision. I'm looking at NYMEX prices for natural gas contracts at Henry Hub in 2025, 2026 and 2027. This is one of the most heavily traded futures markets in the world, and while this information cannot answer all questions, these prices provide a lot of information about where buyers and sellers believe the market is headed.

This is particularly relevant because some of the discussion about the LNG pause has focused on potential impacts for U.S. natural gas consumers. Biden's press release mentions that one of the potential impacts of LNG exports is “energy cost increases for American consumers and manufacturers,” and consumer advocates hail the pause as an important step toward “reducing economic pressure on low-income families.”

When was information revealed?

A major challenge in analyzing the market impact of these types of events is figuring out exactly when information was released. When it comes to raw material prices, all available information – official and unofficial – is given priority. Therefore, it is not enough to know when a policy will be implemented, but it is also necessary to ask whether the change in the policy was expected.

In this case, there's pretty good evidence that the break was a surprise. The White House announced the decision on January 26th. On the same day, the New York Times and the Wall Street Journal published major articles about the decision. I see some related media discussions in the days leading up to the announcement, but nothing before that.

So I'll use the week of January 26th as the “start date” for the break. I don't want to say that the decision came as a complete surprise. Critics have long argued against LNG exports, but until the week of January 26, it was not clear that such a pause would ever occur.

Prices for 2025, 2026 and 2027

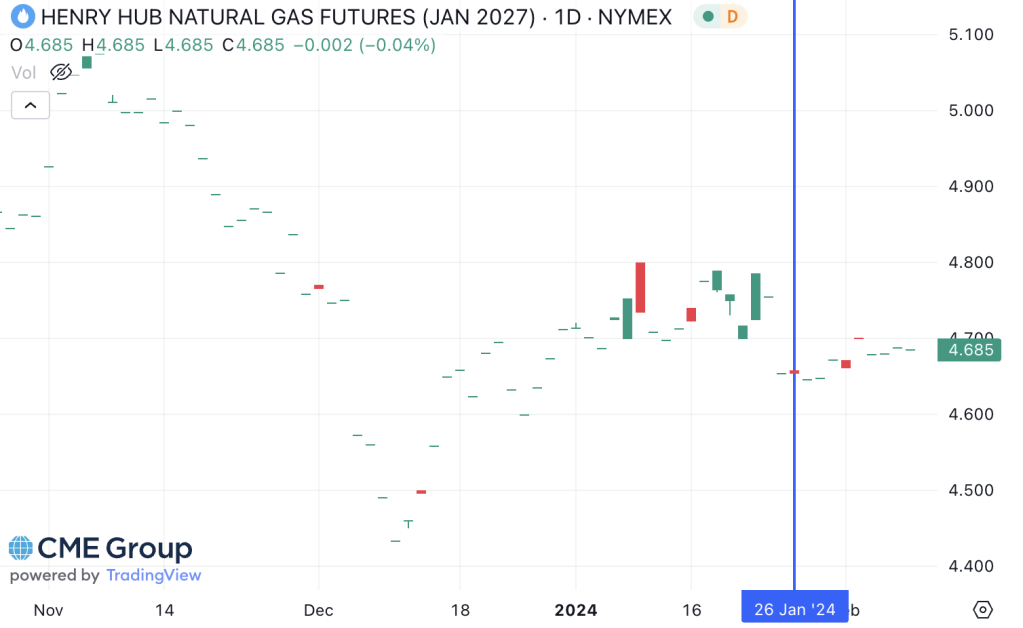

The following figure shows the contracted prices for natural gas deliveries in January 2025. Each observation is a day.

- Green indicates a day when the price increased

- Red indicates a day when the price fell

- Thick bars show opening and closing prices

- Thin bars show high and low prices

The vertical blue line indicates January 26th. There is essentially no change before and after the pause announcement. Prices fluctuate from day to day but remain essentially unchanged during the week of January 26th.

—

The evidence below for contracts delivered in January 2026 and 2027 is similar. The further you go, the lower the transaction volume. A dash indicates that the contract was not traded that day. But in all cases, prices remain essentially unchanged during the week of January 26th.

—

—

Why didn't gas prices respond to the LNG announcement?

I think this shows us that the supply of natural gas is very elastic. Particularly in the medium and long term, there is considerable scope for U.S. natural gas producers to significantly alter their supply in response to even relatively small price changes. We already knew that somehow. U.S. natural gas reserves have increased steadily since 2000, and much of it is accessible at relatively low marginal cost.

The LNG pause represents a potentially sharp decline in future demand for U.S. natural gas. There are currently 17 natural gas export projects nationwide applying for permits, and the pause puts these projects in uncertainty. If we assumed that supply was inelastic, we would expect this leftward shift in the demand curve to push prices sharply downward. But that's not what we're seeing in the futures market. Futures prices changed little, which would be expected if supply was highly elastic.

I would like to highlight two caveats. Firstly, the timing. These futures markets only provide information for the next few years. The break affects facilities that could have started operating during this period. For example, the Calcasieu Pass 2 project, which is affected by the pause, was expected to begin operations in the second quarter of 2025. In addition, markets are linked to each other in time through storage and production decisions, so it would be unusual, for example, that no change is expected in 2027, but major impacts are expected in the following years. Nevertheless, one could argue that the impact on consumers is indeed coming, but that it will not materialize until the end of the decade.

Second, it could simply be that the market doesn't believe the pause will last. At a Senate hearing on February 8, Senator Murkowski suggested that the Department of Energy's review would “conveniently not be completed before the election.” However, it could well be that market participants expect an “unpause” in LNG shortly after the election. I'm an economist, not a political scientist, so I won't speculate on this other than to say that this alternative explanation would fit futures market data.

The evidence here is inconclusive. But I think it's suggestive. The lack of change in the futures market suggests to me that the impact on U.S. natural gas consumers over the next few years will likely be quite modest, regardless of what happens with the LNG pause.

—

Follow us on Bluesky and LinkedIn and subscribe to our email list to stay up to date on future content and announcements.

Suggested citation: Davis, Lucas. “What Can Futures Markets Tell Us About Biden’s LNG Pause?” Energy Institute Blog, February 12, 2024.

Comments are closed.