zimmytws/iStock via Getty Images

The market for high-growth companies that do not generate profits has collapsed this year fly wire (NASDAQ:FLYW) is still aggressively priced. The company completed a hot IPO back in 2021, and this appears to be to blame expanded valuation of the stock this year. my investment thesis remains neutral on the fast-growing payments company.

Large untapped market

The digital payments company plays in markets with a TAM of over $11 trillion in annual payments. The biggest opportunity lies in the B2B payments sector, where TAM exceeds $10 trillion globally. Investors tend to focus more on global e-commerce payments, but the B2B sector is far larger.

Source: Flywire ’22 Investor Day

A prime example of untapped markets, Flywire has less than 1% coverage in most major verticals. These industries have strong growth drivers as the B2B market shifts towards e-invoicing at a 20% growth rate.

Amazingly, Flywire forecasts an opportunity to increase revenue at least fivefold by expanding with existing customers and products. The tremendous opportunity comes from adding customers and building new industries with scalable cloud technology and software tailored to specific use cases. The company offers the ability to offer payment plans for the education sector or multi-party payments for the travel industry, providing the flexibility to meet specific industry needs.

In its most recent quarter, Flywire processed just $2.9 billion in total payment volume, up from $1.9 billion a year earlier. The paytech continued on its path of nearly 50% volume growth, but Flywire has a very small slice of global payments volume, with the bulk of its business centered on the cross-border education system. The Company does not forecast non-educational revenues that will exceed 50% of total revenues for up to 5 years.

Sectors generally survived the COVID shutdowns and even travel is now returning to pre-COVID levels. As in most sectors, COVID accelerated the need for financial automation and digitalization offered by Flywire.

Still valued like an IPO

Like most stocks, Flywire has fallen from its highs over the past year. The stock is now trading below $25 after surging above $50 last October following its successful IPO priced at $24 last May.

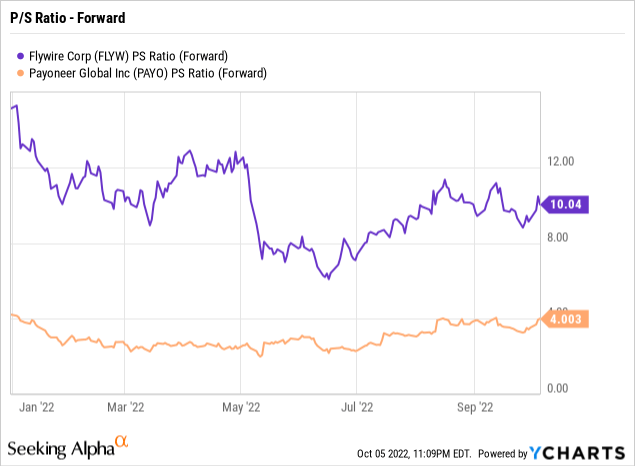

Even a year later, and down 50% from its highs, Flywire still trades at a premium valuation. The stock valuation compared to Payoneer Global (PAYO) is a great example of how the market has treated IPOs versus SPACs. Flywire still trades at 10x futures turnover, while Payoneer only hits 4x turnover targets.

Data from YCharts

Data from YCharts

Recall that Flywire reported a loss of $6 million in EBITDA for the second quarter and is only forecasting adjusted EBITDA of around $15 million for 2022. The market isn’t as impressed with companies struggling to make only EBITDA profits and prefer actual profits.

The paytech company expects revenue of around $265 million in 2022 on growth of 45%. In normal markets, investors definitely love the consistent growth rates of global payments companies, but this is not a normal market.

The company, which focuses on the education payments industry, has quarterly sales with outsized numbers in September. Sometimes this confuses investors and leads to weakness in the stock.

Flywire forecast Q3 22 revenue of at least $87 million compared to just $52 million in the previous quarter. Analysts are forecasting strong Q4 22 revenue of $67 million, but the number is a huge sequential decline. Such a scenario can confuse the investment community as they view this sequential sales decline as a warning against normal seasonal trends.

Truist analyst Andrew Jeffrey recently began coverage of Flywire with a buy rating with a price target of $36. The market is remarkably bullish on the stock despite the lackluster momentum. However, the upside target is just 44% above the current price and well below the post-IPO highs.

Bring away

The key takeaway for investors is that the stock simply doesn’t have much upside potential in the current environment. Investors should definitely keep Flywire on their watch lists due to its attractive growth rates and massive opportunity in its targeted payments industries. The stock just isn’t cheap enough to buy in a market where other stocks have been decimated in what’s typically viewed as a premium valuation multiple.

Comments are closed.