The Federal Reserve is widely expected to slow the pace of its rate-hiking cycle on Wednesday, but the key question is whether it will hint that a pause may be imminent after its next meeting in March.

S

Since the start of the current global tightening cycle, the Fed has been the most aggressive central bank in the G10 alongside the Bank of Canada and has hiked interest rates by a total of 425 basis points. However, we have started to see clear signs of a downtrend in almost every measure of US inflation over the last few months, and there is a general consensus that policymakers may soon be nearing the stage where they are signaling a pause in the hike process is on the way. We don’t think the Fed is there yet, although we do think a return to a smaller 25bp rate hike at this week’s meeting is all but certain.

Ahead of Wednesday’s announcement, financial markets are fully pricing in a 25 basis point move, with more than 80% priced in for another hike of the same magnitude in March. We believe this was relatively well-telegraphed by Fed officials during their pre-blackout days of communications. Most FOMC members have adopted a more dovish tone of late, with a handful, most recently Waller and Brainard, acknowledging that progress has been made on inflation and that the time was right for the pace of hikes to slow. At its last meeting in December, the Fed hiked rates by 50 basis points but refrained from an explicit dovish stance.

Clearly, the main reason for the Fed’s dovish stance was the cooling of US inflationary pressures. While we take the recent fall in headline inflation as encouraging, we see this largely as a result of the sharp fall in energy prices. In our opinion, the downtrend seen in core inflation is a far more telling development, and we think FOMC members will give it more importance. Our favorite metric, the three-month annualized rate of core CPI inflation, fell to just 3.1% in December, its lowest since September 2021. The December reading for the Fed’s favorite metric of price growth, the core PCE index, also ticked lower to 4.4%, which is an equally encouraging step in the right direction.

Exhibit 1: US Core Inflation Rate (2013 – 2022)

Source: Refinitiv Datastream Date: 01/30/2023

We expect Chairman Powell to acknowledge this easing in price pressures on Wednesday and cite it as a key reason for a less aggressive approach. The Fed may also acknowledge the slight deterioration in a handful of economic indicators, most notably consumer spending, while reiterating the possibility of a recession – some officials may see as a prerequisite for bringing inflation down on a sustained basis.

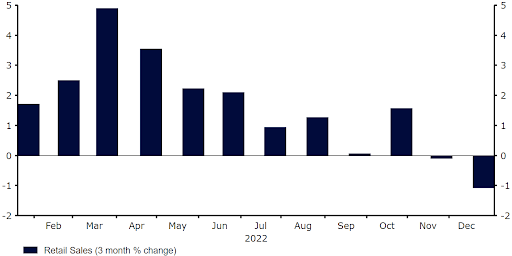

We continue to argue that any downturn will be rather mild, particularly given the resilience of the US labor market, which continues to be characterized by solid job creation and low unemployment. That assumption was bolstered by strong Q4 GDP numbers (+2.9% YoY), December durable goods orders (+5.6% MoM) and weekly initial jobless claims (an 8-month low of 186,000) supported, all exceeding expectations.

Figure 2: US retail sales [3 month % change] (2021 – 2022)

Source: Refinitiv Datastream Date: 01/30/2023

The Fed will not release any macroeconomic or rate forecasts this week, with the next dot plot not due until the bank’s March meeting. We believe the US dollar’s reaction will therefore depend almost entirely on the Fed’s accompanying rhetoric, including Chair Powell’s press conference. The key question will be whether the Fed is hinting that a rate pause is imminent. Should the bank adjust its language regarding the need for “ongoing hikes” in the Fed Funds rate, it could signal a pause in the rate hike cycle after the March meeting. In our view, this would be considered bearish for the dollar and could extend the currency’s recent move lower against most currencies.

However, as in December, the Fed could again keep its options open and potentially leave the door open to an additional, final hike of 25 basis points in May should upcoming data warrant it. While this would be consistent with the Fed’s December ‘dot plot’, we believe this would likely be perceived as bullish for the US dollar as it is more aggressive than currently being priced by financial markets. At the very least, we think Powell will emphasize that there is still work to be done as Fed members may wish to see extended wage easing before taking their foot off the pedal completely.

Figure 3: Average US Hourly Earnings (2013 – 2022)

Source: Refinitiv Datastream Date: 01/30/2023

For the time being, we again expect Powell to scale back expectations for any rate cuts in the near future. As of this writing, futures markets are pricing in the first cut in November, which we find a bit hasty, if not entirely impossible, even at this early stage. After the Fed’s December meeting, Chairman Powell noted that he did not foresee any easing of monetary policy until the committee was “confident of inflation falling to 2 percent on a sustainable basis.”

We suspect Powell will reiterate this view during this week’s press conference, although we believe the Fed’s stance on future rate hikes will be more relevant to currencies for now. As things stand, we are targeting a final 25 basis point hike in March, although this could change if US inflation does not weaken as expected.

The FOMC will announce its latest policy decision at 18:00 GMT (19:00 CET) on Wednesday, followed by Chairman Powell’s press briefing 30 minutes later.

Comments are closed.