Drew Angerer

introduction

As you probably all know, last week the Fed announced that rates would rise by 0.75% for the third consecutive month.

Fed Chair Powell’s comments were seen as extremely hawkish in general and about inflation in particular. That sent a shiver down the spine of the stock market and the shares fell like a stone.

Data from YCharts

Data from YCharts

Growth forecasts were revised downwards, the unemployment outlook suddenly looked bleaker and it was repeatedly said that a painful recession would be needed to halt high inflation.

Economists at Goldman Sachs and Barclays now expect another rate hike of 0.75% in November, 0.50% in December and 0.25% in February. This can lead to a peak of 4.5% to 4.75%, 0.5% higher than before the session.

Of course, no matter what the Fed does, there will always be criticism. So to speak, millions of people think they’re doing a better job, and while some may be right, there’s no denying that the Fed has some of the brightest macroeconomists in its ranks. But the main question is: is the Fed doing what it should or is it killing the economy?

Professor Jeremy Siegel is angry

Wharton Professor Jeremy Siegel believes the Fed is doing a very, very bad job and is way too strict. He’s upset. He summarizes: the strongest dollar in decades, falling asset prices, the rapidly declining M2 supply and falling commodity prices. His conclusion is clear:

We don’t have to get close to that level to stop inflation. (…) I think the Fed is just way too tight.

There is indeed a lot of economic data that suggests inflation is stalling. The professor looks forward to the Case-Shiller data next week, which tracks house prices. My wife used to be an attorney in the industry, and from what I’m hearing from people we know in the industry, it would be a huge surprise if the Case-Shiller data didn’t confirm that house prices are falling and sink fast.

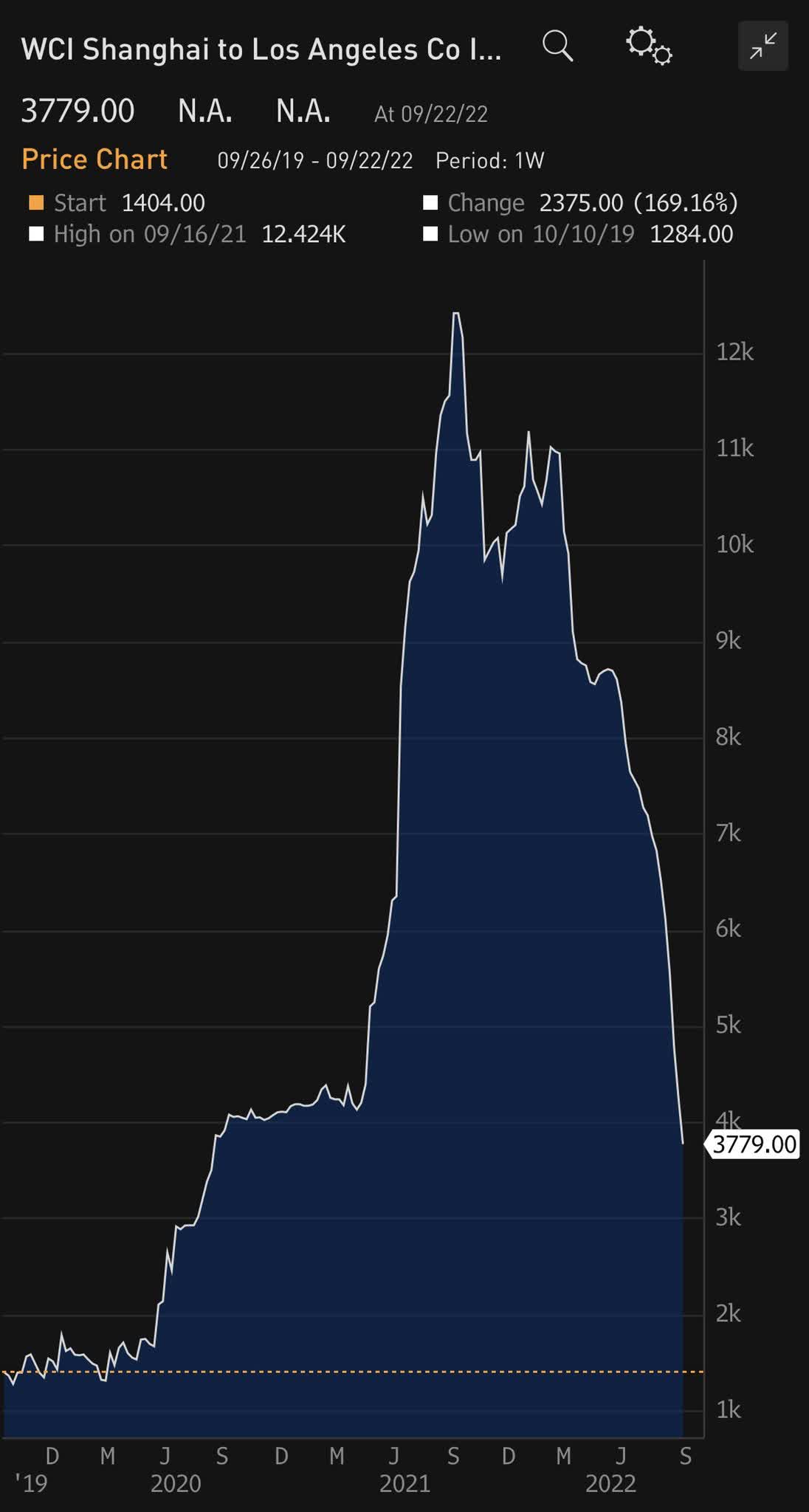

Another indicator that could suggest inflation is coming down fast, Siegel says, is shipping. The shipping costs fell like a stone.

(Source)

As we all know and have experienced, inflation has inflated building materials, chips, car parts, bikes, toys and so many other things. Part of this could be attributed to extremely high shipping prices since the pandemic began. But now prices are crashing, down 16% in the last week alone and at a 2-year low. Consumer prices are a lagging factor, as are wages. They follow the prices of basic materials, raw materials, transport and so on, but only months later. Siegel points this out passionately. The data shows that all costs are falling, and Siegel believes this shows that inflation is already broken. The implication is that being too strict now doesn’t break inflation, it breaks people’s backs.

This is another indicator that Siegel may be right.

(Source)

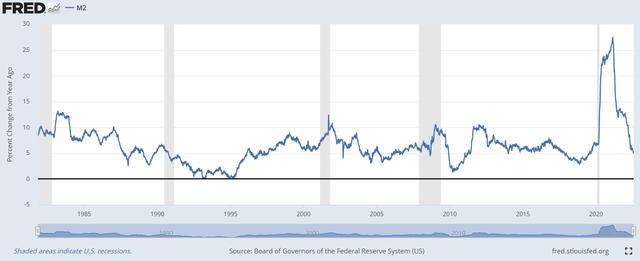

Siegel also referred to the M2. You could compare M2 to cash and equivalents on a balance sheet. M1 is cash and everything related to current deposits, while M2 also includes savings accounts, term deposits, and money market accounts. In other words, when you transfer money from your savings account to your checking account, you have transferred money from M2 to M1. M1 will increase but M2 stays the same as it contains M1. This is the M2 YoY growth chart.

fred

While households have saved a lot more money during the pandemic, you can see that this has already fallen sharply. M2 is considered the leading indicator of inflation, although as with many economic indicators, there are some doubts about it too.

Elon Musk was quick to point out that Siegel was correct in his assessment.

Who is right? Siegel or the Fed?

It is very clear to me that Siegel has a very strong case here. To subscribers to my marketplace, Potential Multibaggers, I have shared dozens of similar data points that suggest inflation is likely to fall quickly soon.

Maybe, and this is a very wild guess, maybe even the Fed agrees with what Siegel is saying to some degree. But the Federal Reserve and its chairman are caught between a rock and a hard place. Any single word that could be construed as slightly dovish would send this highly volatile market skyrocketing, and that’s exactly what they want to avoid. Therefore, his public hawkishness can play a crucial role. It’s a dangerous game, but it might be a necessary game for a while. The problem is we don’t know, and playing this game for too long can be bad for the economy and ultimately for all of us. I think we’ll have to see how that develops.

The result for investors

What is the outcome for investors? Well, to start with.

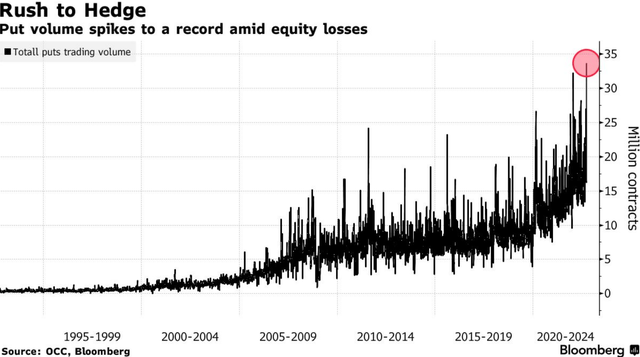

Bloomberg

(Source)

The highest put volume ever was traded on Friday. This may sound scary as it is very bearish. But one of the things I like about this chart is its large scope. Look at the highest peaks and what you see every time are excellent opportunities for long-term investors: the March 2020 Covid crash, the euro crises, the Great Recession and so on. Of course, this also has to do with more and more trading, which by nature is short-term oriented.

Those who invest for the long term have an advantage. But having an advantage isn’t easy. You have to be willing to look silly for a long time to be successful. We are in such a time, and that time may not be over anytime soon. It could be months or even longer before we are out of this dire situation. But if you’re in the accumulation phase of your investing journey, I think it’s a good time to put money in regularly, even if the markets are still falling for a longer period of time.

Conclusion

The Fed may be exaggerating its hawkish stance, but it doesn’t want to take any chances. I think that’s probably even smart. As Siegel pointed out, the Fed should have raised rates sooner. Now that they’ve made that mistake, they can’t make a second one to let inflation spiral out of control. To salvage future prosperity, the Fed must stop this high inflation at all costs, even if it is too severe and is causing a deep wound in our economy. Let’s just hope he has the flexibility to change his decisions if inflation did indeed come down quickly.

In the meantime, keep growing!

Comments are closed.